Survey Says Subprime and Credit Top Short-Term Threats to U.S. Economy

Location: Washington

Author:

Catherine Mann, Richard Brown & Kathleen Camilli

Date: Tuesday, August 28, 2007

The combined threat of subprime loan defaults and excessive indebtedness has supplanted terrorism and the Middle East as the biggest short-term threat to the U.S. economy. Just 20 percent of NABE members surveyed listed terrorism and the Middle East as their top concern in August, compared to 35 percent in March. Meanwhile, 18 percent of those surveyed pointed to the effects of the subprime debacle as their biggest concern, and the related issue of “excessive household and/or corporate debt” was cited by another 14 percent.

|

Short-Term Risks to the US Economy (Percent of survey panelists responding) |

|||||

|

|

Survey Date |

||||

|

|

Sep 05 |

Mar 06 |

Aug 06 |

Mar 07 |

Sep 07 |

| Combined subprime default & debt |

na |

na |

na |

na |

32 |

| Effects of subprime loan defaults |

na |

na |

na |

na |

18 |

| Excessive household/corporate debt |

9 |

7 |

5 |

13 |

14 |

| Defense/terrorism |

20 |

26 |

34 |

35 |

20 |

| Energy Prices |

30 |

23 |

29 |

9 |

13 |

| Current account deficit |

11 |

13 |

11 |

12 |

8 |

| Inflation |

5 |

3 |

12 |

4 |

6 |

| Employment issues |

1 |

1 |

1 |

7 |

5 |

| Govt spending/ deficit |

13 |

14 |

2 |

5 |

3 |

The most serious long-term challenges facing the U.S. economy are health care costs, cited by 24 percent of respondents, and an aging population, cited by 21 percent.These responses were similar to survey rankings from 2005 and 2006. Education and skilled labor rank close behind, with 17 percent seeing them as the nation’s most important long-term challenge.

|

Longer-Term Challenges to the US Economy (Percent of survey panelists responding) |

|||||

|

|

Survey Date |

||||

|

|

Sep 05 |

Mar 06 |

Aug 06 |

Mar 07 |

Sep 07 |

| Health care |

23 |

22 |

16 |

25 |

24 |

| Growth of elderly population/dependency ratio |

18 |

21 |

17 |

23 |

21 |

| Education system |

21 |

16 |

21 |

15 |

17 |

| Federal deficit |

22 |

22 |

23 |

19 |

13 |

| Energy issues |

4 |

8 |

13 |

8 |

9 |

| Competitiveness |

7 |

5 |

4 |

4 |

6 |

The ranking of U.S. economic strengths remains unchanged, led by labor force flexibility (39 percent), technology and productivity (24 percent), and deep capital markets (15 percent).

|

US Economic Strengths (Percent of survey panelists responding) |

|||||

|

|

Survey Date |

||||

|

|

Sep 05 |

Mar 06 |

Aug 06 |

Mar 07 |

Sep 07 |

| Flexible labor markets/economy |

42 |

35 |

39 |

38 |

39 |

| Productivity/technology |

26 |

29 |

27 |

27 |

24 |

| Deep capital markets |

11 |

16 |

18 |

17 |

15 |

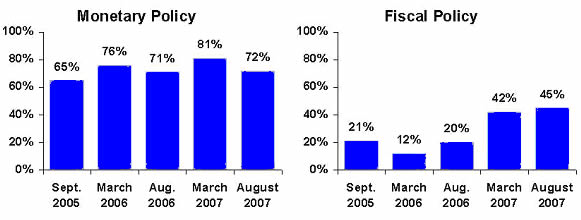

The consensus on monetary policy was beginning to fray even before the survey ended on August 14. The percent of respondents judging monetary policy to be “about right” slipped to 72 percent in August from 81 percent in March, while those calling policy “too restrictive” almost doubled to 16 percent. A plurality (47 percent) of NABE members continue to call U.S. fiscal policy “too stimulative,” although the 45 percent who think it is “about right” is more than twice as large as a year ago.

Percent of NABE Panelists Who Consider Current Policy to be "About Right"

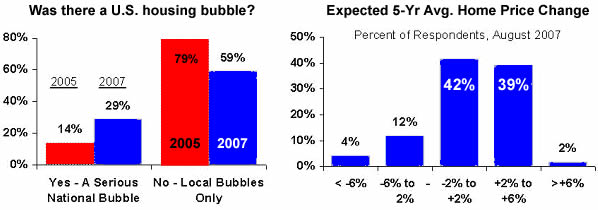

Interpretations of the early-2000s U.S. housing boom have shifted. Responding to a series of questions first asked in the August 2005 Policy Survey, more NABE members now view the boom as a credit-induced bubble. Just over 29 percent now call the boom a “serious national bubble,” compared to only 14 percent two years ago. Virtually all of this increase came from the group of respondents who previously ascribed the trend to “local bubbles.” The percentage citing “easier credit standards” as the number one or number two cause for the housing boom jumped to 64 percent from 34 percent in 2005. Just over 60 percent of NABE members polled agreed that the new mortgage lending rules issued by federal banking regulators are “necessary and appropriate;” however, among these supporters a vast majority (over 90 percent) also termed the action “a little late.”

The five-year housing outlook remains largely positive. A slight plurality (42 percent) of respondents expects U.S. home prices to be flat, on average, over the next five years. But respondents who expect home prices to rise on average over the next five years (41 percent) far outnumber those who expect prices to fall (16 percent). NABE members continue to place low odds (1 in 10) on a large drop in U.S. home prices similar to that experienced in Japan during the 1990s.

Substantial percentages of economists report little familiarity with complex instruments and other financial innovations. Despite the prevalence of NABE members holding advanced degrees in economics and other business-related disciplines, substantial percentages admitted to having little or no familiarity with the structure, activities, and risks associated with hedge funds (45 percent), private equity funds (40 percent), asset-backed securitization (48 percent), credit default swaps (CDS, 68 percent and collateralized debt obligations (CDOs, 51 percent).

The greatest threat to financial stability is thought to arise from CDOs, followed by hedge funds and CDS. In terms of regulation and reporting requirements, members were generally split between “fine as is” and “prefer more,” with the greatest need for regulatory and reporting enhancements seen for hedge funds (57 percent) and CDOs (48 percent). More than six out of ten those surveyed agreed that the “carried interest” gains earned by partners in private equity funds should be taxed as ordinary income.

NABE members are divided as to their assessment of the threat posed by man-made global warming. Some 53 percent of respondents accept man-made global warming due to CO2 emissions as a “fact.” Of these, just over four-fifths also agree that the problem poses “significant risks that must be addressed immediately.” On the other side of the ledger, 45 percent do not yet accept man-made global warming as a fact, although two-thirds of that number state that further study of the issue is needed.

The most popular policy prescription for reducing man-made carbon emissions is higher fuel economy standards for cars and trucks. Close behind are proposals for a “carbon tax” or a system for capping emissions and trading carbon credits. A vast majority (93 percent) of respondents agreed that much could potentially be done to reduce man-made carbon emissions using current technologies, and 44 percent feel that significant gains could be made at relatively low cost.

To subscribe or visit go to: http://www.riskcenter.com