IEA's Report on 1st- to 2nd-Generation Biofuel Technologies

The current debate over biofuels produced from food crops has pinned a lot of hope on "2nd-generation biofuels" produced from crop and forest residues and from non-food energy crops. This IEA report, produced jointly with IEA Bioenergy, examines the current state-of-the-art and the challenges for 2nd-generation biofuel technologies. It evaluates their costs and considers policies to support their development and deployment.

It is increasingly understood that 1st-generation biofuels produced primarily from food crops are limited in their ability to achieve targets for oil-product substitution, climate change mitigation and economic growth. Their sustainable production is under review, as is the possibility of creating undue competition for land and water used for food and fiber production. A possible exception that appears to meet many of the acceptable criteria is ethanol produced from sugar cane.

The cumulative impacts of these concerns have increased the interest in developing biofuels produced from non-food biomass. These "2nd-generation biofuels" could avoid many of the concerns facing 1st-generation biofuels and potentially offer greater cost reduction potential in the longer term.

Our recent IEA report looks at the technical challenges facing 2nd-generation biofuels, evaluates their costs and examines related current policies to support their development and deployment. The potential for production of more advanced biofuels is also discussed. Policy recommendations are given as to how these constraints to commercial deployment might best be overcome in the future.

While most analyses continue to indicate that 1st-generation biofuels show a net benefit in terms of GHG emissions reduction and energy balance, they also have several drawbacks. Current concerns for many, but not all, of the 1st-generation biofuels are that they:

-

contribute to higher food prices due to competition with food crops;

-

are an expensive option for energy security taking into account total production costs excluding government grants and subsidies;

-

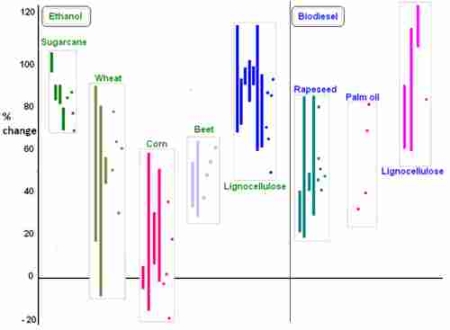

provide only limited GHG reduction benefits (with the exception of sugarcane ethanol, Fig. 1) and at relatively high costs in terms of $/tonne of carbon dioxide ($/t CO2) avoided;

-

do not meet their claimed environmental benefits because the biomass feedstock may not always be produced sustainably;

-

are accelerating deforestation (with other potentially indirect land use effects also to be accounted for);

-

potentially have a negative impact on biodiversity; and

-

compete for scarce water resources in some regions.

Additional uncertainty has also recently been raised about GHG savings if indirect land use change is taken into account.

Second Generation Biofuels

Many of the problems associated with 1st-generation biofuels can be addressed by the production of biofuels manufactured from agricultural and forest residues and from non-food crop feedstocks. Where the ligno-cellulosic feedstock is to be produced from specialist energy crops grown on arable land, several concerns remain over competing land use, although energy yields (in terms of GJ/ha) are likely to be higher than if crops grown for 1st-generation biofuels (and co-products) are produced on the same land. In addition poorer quality land could possibly be utilized.

Given the current investments being made to gain improvements in technology, some expectations have arisen that, in the near future, these biofuels will reach full commercialization. This would allow much greater volumes to be produced at the same time as avoiding many of the drawbacks of 1st-generation biofuels. However, from this IEA analysis, it is expected that, at least in the near to medium-term, the biofuel industry will grow only at a steady rate and encompass both 1st- and 2nd-generation technologies that meet agreed environmental, sustainability and economic policy goals.

The transition to an integrated 1st- and 2nd generation biofuel landscape is therefore most likely to encompass the next one to two decades, as the infrastructure and experiences gained from deploying and using 1st-generation biofuels is transferred to support and guide 2nd-generation biofuel development.

Conversion Routes

The production of biofuels from ligno-cellulosic feedstocks can be achieved through two very different processing routes both currently at the demonstration phase.

-

Biochemical — in which enzymes and other micro-organisms are used to convert cellulose and hemicellulose components of the feedstocks to sugars prior to their fermentation to produce ethanol;

-

Thermo-chemical — where pyrolysis/gasification technologies produce a synthesis gas (CO + H2) from which a wide range of long carbon chain biofuels, such as synthetic diesel or aviation fuel, can be reformed.

These are not the only 2nd generation biofuels pathways, and several variations and alternatives are under evaluation in research laboratories and pilot-plants including dimethyl ether, methanol or synthetic natural gas. However, at this stage these alternatives do not represent the main thrust of RD&D investment.

Based on the announced plans of companies developing 2nd-generation biofuel facilities, the first fully commercial-scale operations could possibly be seen as early as 2012 if demonstrations prove successful. However given the complexity of the technical and economic challenges involved, in reality, the first commercial plants are unlikely to be widely deployed before 2020.

Preferred Technology Route

There is currently no clear commercial or technical advantage between the two pathways, even after many years of RD&D and the development of near-commercial demonstrations. Both sets of technologies remain unproven at the fully commercial scale, are under continual development and evaluation, and have significant technical and environmental barriers yet to be overcome.

For the biochemical route, much remains to be done in terms of improving feedstock characteristics; reducing the costs by perfecting pretreatment; improving the efficacy of enzymes and lowering their production costs; and improving overall process integration. The potential advantage of the biochemical route is that cost reductions have proved reasonably successful to date, so it could possibly provide cheaper biofuels than via the thermo-chemical route.

Conversely, as a broad generalization, there are less technical hurdles to the thermo-chemical route since much of the technology is already proven. One problem concerns securing a large enough quantity of feedstock for a reasonable delivered cost at the plant gate in order to meet the large commercial-scale required to become economically viable (Table 1). Also perfecting the gasification of biomass reliably and at reasonable cost has yet to be achieved, although good progress is being made.

Table 1 shows the typical scale of operation for various 2nd-generation biofuel plants using energy crop-based ligno-cellulosic feedstocks.

|

Type of plant |

Plant capacity ranges, and assumed annual hours of operation. |

Biomass fuel required. (oven dry tonnes / year) |

Truck vehicle movements for delivery to the plant. |

Land area required to produce the biomass. (% of total land within a given radius). |

|

Small pilot |

15,000-25,000 l/yr 2000 hr |

40-60 |

3 - 5 / yr |

1 - 3% within |

|

Demonstration |

40,000-500,000 l/yr 3000 hr |

100-1200 |

10 - 140 / yr |

5 - 10% within |

|

Pre-commercial |

1-4 M l/yr |

2,000-10,000 |

25 - 100 / month |

1 - 3% within |

|

Commercial |

25-50 M l/yr 5000 hr |

60,000-120,000 |

10 - 20 / day |

5 - 10% within |

|

Large commercial |

150-250 M l/yr |

350,000-600,000 |

100 - 200 / day and night |

1-2% within |

Note: The land area requirement would be reduced where crop and forest residue feedstocks are available.

One key difference between the biochemical and thermo-chemical routes is that the lignin component is a residue of the enzymatic hydrolysis process and hence can be used for heat and power generation. In the BTL process it is converted into synthesis gas along with the cellulose and hemicellulose biomass components. Both processes can potentially convert 1 dry tonne of biomass (~20 GJ/t) to around 6.5 GJ/t of energy carrier in the form of biofuels giving an overall biomass to biofuel conversion efficiency of around 35%. Although this efficiency appears relatively low, overall efficiencies of the process can be improved when surplus heat, power and co-product generation are included in the total system.

Although both routes have similar potential yields in energy terms, different yields, in terms of liters per tonne of feedstock, occur in practice. Typically enzyme hydrolysis could be expected to produce up to 300 l ethanol / dry tonne of biomass whereas the BTL route could yield up to 200 l of synthetic diesel per tonne but with a higher energy density by volume.

A second major difference is that biochemical routes produce ethanol whereas the thermo-chemical routes can also be used to produce a range of longer-chain hydrocarbons from the synthesis gas. These include biofuels better suited for aviation and marine purposes. Only time will tell which conversion route will be preferred, but whereas there may be alternative drives becoming available for light vehicles in future (including hybrids, electric plug-ins and fuel cells), such alternatives for airplanes, boats and heavy trucks are less likely and liquid fuels will continue to dominate.

Production Costs

The full biofuel production costs associated with both pathways remain uncertain and are treated with a high degree of commercial propriety. Comparisons between the biochemical and thermo-chemical routes have proven to be very contentious within the industry, with the lack of any real published cost data being a major issue for the industry.

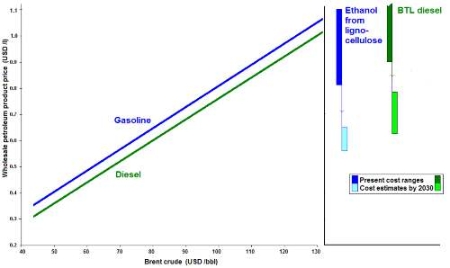

The commercial-scale production costs of 2nd-generation biofuels have been estimated by the IEA to be in the range of US $0.80 - 1.00/liter of gasoline equivalent (lge) [US $3.02-$3.79 per gallon] for ethanol and at least US $1.00/liter [$3.79 per gallon] of diesel equivalent for synthetic diesel. This range broadly relates to gasoline or diesel wholesale prices (measured in USD /lge) when the crude oil price is between US $100-130 /bbl (Fig. 2). The present widely fluctuating oil and gas prices therefore make investment in 2nd-generation biofuels at current production costs a high risk venture.

If commercialization succeeds and rapid deployment occurs world-wide beyond 2020, then costs could decline to between US $0.55 and 0.60/lge [US $2.08 - $2.27 per gallon] for both ethanol and synthetic diesel by 2030. Ethanol would then be competitive at around US $70/bbl (2008 dollars) and synthetic diesel and aviation fuel at around US $80/bbl.

Implications for Policies

Promotion of 2nd-generation biofuels can help provide solutions to multiple issues including energy security and diversification, rural economic development, GHG mitigation and help reduce other environmental impacts (at least relative to those from the use of other transport fuels). Policies designed to support the promotion of 2nd-generation biofuels must be carefully developed if they are to avoid unwanted consequences and potentially delay commercialization.

One related view is that the relatively high cost of support currently offered for many 1st-generation biofuels is an impediment to the development of 2nd-generation biofuels, as the goals of some current policies that support the industry (with grants and subsidies for example) are not always in alignment with policies that foster innovation.

This report leans more towards the position that advances in technology will enable 2nd-generation biofuels to build on the infrastructure and markets established by 1st-generation biofuels but will provide a cheaper and more sustainable alternative. This assumes that future policy support will be carefully designed in order to foster the transition from 1st- to 2nd- generation and take into account the specificities of 1st- and 2nd- generation biofuels, the production of sustainable feedstocks, and other related policy goals being considered.

Key points are that:

-

policies to support 1st- or 2nd-generation biofuels should be part of a comprehensive strategy to reduce CO2 emissions;

-

enhanced RD&D investment in 2nd-generation biofuels is needed;

-

accelerating the demonstration of commercial-scale 2nd generation biofuels in different regions is required;

-

deployment policies for 2nd-generation biofuels are either blending targets or tax credits; and

-

environmental performance and certification schemes need to be developed.

Conclusions

The key messages arising from the study are:

-

technical barriers remain for 2nd-generation biofuel production;

-

production costs are uncertain and vary with the feedstock available, but are currently thought to be around US $0.80 - 1.00/liter [US $3.02-$3.79 per gallon] of gasoline equivalent;

-

there is no clear candidate for "best technology pathway" between the competing biochemical and thermo-chemical routes;

-

the development and monitoring of several large-scale demonstration projects is essential to provide accurate comparative data;

-

even at high oil prices, 2nd-generation biofuels will probably not become fully commercial nor enter the market for several years to come without significant additional government support;

-

considerably more investment in RD&D is needed to ensure that future production of the various biomass feedstocks can be undertaken sustainably and that the preferred conversion technologies are identified and proven; and

-

once proven, there will be a steady transition from 1st- to 2nd-generation biofuels (with the exception of sugarcane ethanol that will continue to be produced sustainably in several countries).

Policies designed to reward environmental performance and sustainability of biofuels, as well as to encourage provision of a more abundant and geographically extensive feedstock supply, could see 2nd-generation products begin to eclipse 1st-generation alternatives in the medium to longer-term.

Acknowledgements

With support from the Italian Ministry for the Environment, Land and Sea, the IEA was able to provide this contribution to the program of work of the Global Bioenergy Partnership, initiated by the G8 countries at the 2005 Summit at Gleneagles and with its Secretariat based in Rome at the Food and Agriculture Organisation of the United Nations.

The full 124 page report is available on the IEA website as a free publication download.

Ralph Sims is Professor of Sustainable Energy at Massey University, New Zealand where he began his research career producing biodiesel from animal fats in the early 1970s. He is currently based at the Renewable Energy Unit of the International Energy Agency, Paris. He was the Coordinating Lead Author of the "Energy Supply" chapter of the IPCC 4th Assessment Report and is a Companion of the Royal Society. His many publications on energy and climate change mitigation include the book "The Brilliance of Bioenergy - in Business and in Practice."

The information and views expressed in this article are those of the author and not necessarily those of RenewableEnergyWorld.com or the companies that advertise on its Web site and other publications.

Comment:

Ralph and Michael, I'm with you on most of what you say, but have

problems with this paragraph:

"This report leans more towards the position that advances in technology

will enable 2nd-generation biofuels to build on the infrastructure and

markets established by 1st-generation biofuels but will provide a cheaper

and more sustainable alternative. This assumes that future policy support

will be carefully designed in order to foster the transition from 1st- to

2nd- generation and take into account the specificities of 1st- and 2nd-

generation biofuels, the production of sustainable feedstocks, and other

related policy goals being considered."

First, it begs the question of whether current levels of support to

1st-generation agrofuels are cost-effective. This seems to be suggesting

that the status quo should be maintained. Yet current support policies

differ widely from country to country, both in terms of levels of support

per litre and in their design. For example, in some countries (e.g., Canada)

support is reduced as oil prices rise. In other countries, the subsidies are

the gift that keeps on giving, and continue to be provided no matter what

happens to oil prices.

Also, in terms of the technology, there are vast differences in the value of

innovation taking place in association with different 1st-generation

biofuels and the value of those innovations for 2nd or 3rd-generation

biofuels. Even the U.S. Energy Information Administration has gone record

saying that ethanol production from sugar and starch is a "mature

technology." Most of the R&D and in relation to 2nd-generation plants that

is needed is upstream from the fermentation and distillation stage. How is

support for grain-ethanol plants helping there?

As for biodiesel, there is virtually NO connection between the current

dominant transesterfication process and 2nd-generation processes for

producing synthetic middle distilates. So what's the benefit there?

As for investment in infrastructure, the jury is still out as to whether

the future lies in large volumes of ethanol or of fuels (like octanol or

butanol, and synthetic diesel and aviation fuel) that can work with the

current infrastructure. Yet the more governments invest in ethanol

infrastructure, the more they create a bias in the system towards ethanol.

Moreover, do you really expect many current corn-ethanol plants to convert

to running purely on cellulosic materials, like switchgrass? (If so, that

does not solve the fuel-vs-fuel problem, because arable land would still be

used.) Isn't it more likely that if they do engage in cellulosic ethanol

production it will be as an add on to corn-ethanol production -- e.g., using

corn cobs -- rather than a case of a "transition" to 2nd-generation biofuels?

Finally, you mention that "deployment policies for 2nd-generation biofuels

are either blending targets or tax credits". (Note: many countries use

BOTH.) Is that a recommendation, or an assumption? If the former, was any

consideration given to a carbon tax as an alternative?

Ronald STEENBLIK

Large scale use of land based biomass to supply present global average

energy consumption is physically impossible. As the practical efficiency

from sunlight to biofuel is less than 0.5 %, it requires 3000 square meter

of fertile land per person, which we do not have on this planet. Presently

some 1500 square meter fertile land per person are available for food

production. Furthermore, each liter of biofuel requires on average some 500

liter of water to transpire through the plants to create biomass through

photosynthesis -- wilting plants do not produce. On top of all that biofuels

destroy biodiversity, and the impact on the vital ecosystem integrity are

prohibitive.

By contrast, technical conversion of sunlight is 100 times more efficient,

and requires only 30 square meter of collectors per person to replace

present energy use from fossil fuels, which is technically feasible.

These are the results of a study I published in a peer reviewed journal:

Physics in Canada, Vol. 63, No. 3 (july-Sept. 2007), p. 113.

Helmut Burkhardt

![]() To subscribe or visit go to:

http://www.renewableenergyaccess.com

To subscribe or visit go to:

http://www.renewableenergyaccess.com