Milestone: 10 Gigawatts of PV in 2010, Part 2

As we approach the upcoming autumn milestone of 10 gigawatts of solar installed in 2010, Greentech Media asks a few solar luminaries to reflect on the event. You are welcome to add your voice.

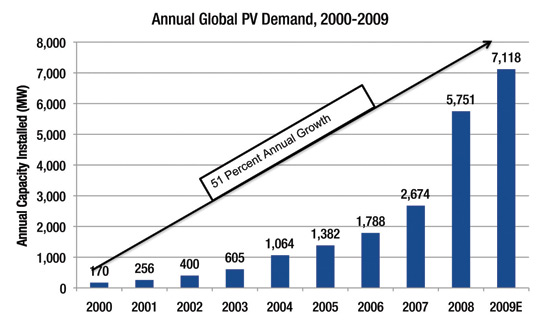

In 2010, we will cross the threshold of 10 gigawatts of photovoltaic solar installed globally in a single year -- a record-setting and once-inconceivable number.

Rewind to ten years ago: the total amount of photovoltaics installed in the year 2000 was 170 megawatts. Since then, the solar photovoltaic industry has grown at a 51 percent annual growth rate, and 170 megawatts is now the size of a healthy utility installation or a small solar factory. As Andrew Beebe mentions below, Suntech has a single building with a one-gigawatt capacity.

Photovoltaic module pricing has made radical progress, as well, moving from $300 per watt in 1956, to $50 per watt in the 1970s, to $10 per watt in the 1990s, to $2 per watt today. It's not exactly Moore's law, but it is that drop in pricing, chicken-or-egg with policy and technology, that is driving this industry. Pricing of $1 per watt is not that far off.

Ten gigawatts is a significant milestone for the PV industry, but it warrants some perspective:

- That's the total power that five or six nuclear power plants generate -- and there are about one hundred nuclear plants in the U.S alone.

- The wind industry installed 27 gigawatts in 2008, 38 gigawatts in 2009 and has a total installed base of more than 158 gigawatts compared to PV's installed base of about 20 gigawatts. 2010 will see more than 200 gigawatts of installed wind and the Global Wind Energy Council expects that to double to 400 gigawatts by the end of 2014.

A few more points about today's PV market: From a demand standpoint, it's healthier, with less reliance on "savior" markets and feed-in tariff hot spots. Note the diminishing reliance on Germany as solar savior in the chart below and get many more details in Shayle Kann's recent PV demand analysis.

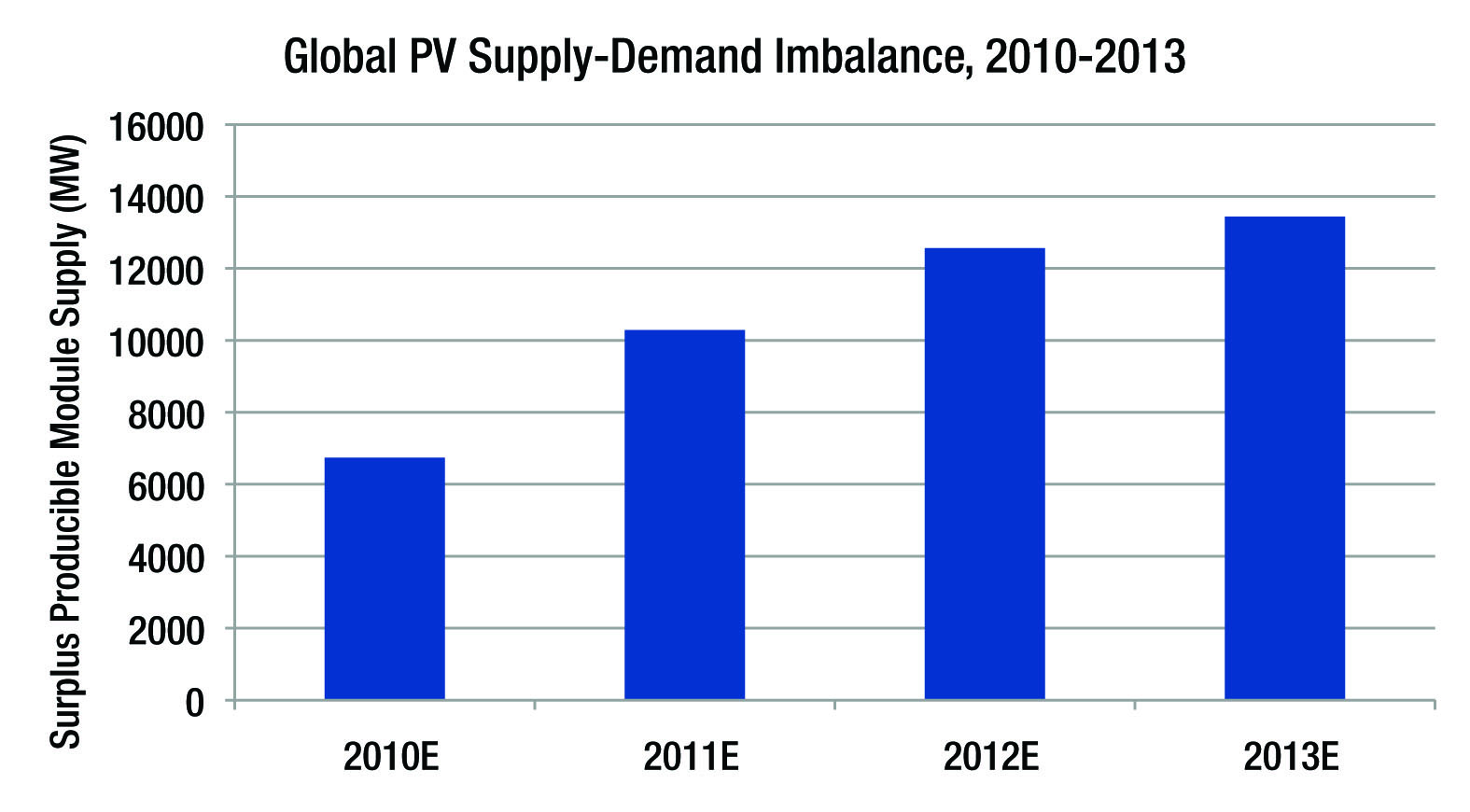

From a supply standpoint, the market is less healthy -- over-supplied and ripe for consolidation.

Still, the 10-gigawatt-PV-installed mark will occur, barring disaster, sometime in October. Our calculations put it at 2:15 PM on October 13. It's a milestone worth noting and a stepping stone, as Jeff Wolfe notes below, on the way to 100 gigawatts installed in 2020.

Here are some reflections on the achievement from some of the technologists, entrepreneurs and investors making it happen:

Steven Strong, President Solar Design Associates

My first ‘big opportunity’ out of engineering school in 1973 was

landing a job working for the oil companies as an engineer on the

Alaskan pipeline. In early October (of 1973), the Arab / Israeli

“Yom Kippur” war broke out and, within days, precipitated the first

world oil embargo. The Western world was broadsided and convulsed

with the stark realization of how dependent we were on OPEC oil. At

that time, the U.S. imported ~15% of its oil -- today that figure is

~70%.

The very next week, as the war raged on and gasoline lines grew in

every Western city, the scientists, engineers and researchers who

had perfected photovoltaics for space-based power systems came

together in Cherry Hill, New Jersey to begin to explore how this

life-affirming technology could be used for terrestrial electric

power. This first world colloquium on “Photovoltaic Conversion of

Solar Energy for Terrestrial Applications” was planned for months

and just happened to take place as the world was gripped by the

first OPEC oil embargo.

The convergence of these two events was an epiphany for me as the

stark contract of these two energy sources and the future they

portended became clear: Clean, Inexhaustible, Free, Life-Affirming

v. Polluting, Finite, Costly and a Devil’s Bargain. I could not

stop thinking about it. The prospect, however nascent, of

leveraging my engineering skills to build a career in solar energy

became increasingly compelling.

As the world price of oil skyrocketed from $3/bbl to over $12, ALYESKA (the pipeline consortium) furiously threw money at the design and construction effort. The pipeline was attractive at $3/ bbl and now ‘their’ Alaskan oil would fetch over four times that amount! It was a heady time in Alaska -- greed stoked with patriotism marshaled a military-like campaign to Get the Pipeline Done and get “our oil to market.” With unlimited overtime and performance bonuses, our weekly pay exceeded most people’s regular monthly salaries.

Was going to the end of the earth to extract the last of the

fossil fuels the best use of my budding skill set? Despite the

bonanza, I resigned from my pipeline position and, not really

knowing any better, founded Solar Design Associates in the spring of

1974 to offer design services in energy-autonomous buildings and the

engineering and integration of the renewable energy systems to power

them. About this same time, Dr. Joseph Lindmeyer was founding

Solarex -- one of the first U.S. PV companies. Crystalline PV was <

$30 / Wp, and the Japanese government inaugurated their “Project

Sunshine,” a high-level, coordinated, 25-year program with the goal

of commercializing PV for widespread, cost-competitive terrestrial

use by the year 2000.

In 1975, the U.S. government authorized NASA’s Jet Propulsion

Laboratory (JPL) and their Lewis Research Center (LeRC) to pursue a

major development program for terrestrial PV, Bill Yerkes launched

Solar Technology International, and Ishaq Shahryar founded Solec

International. Tyco labs grew crystalline EFG ribbon and Exxon

expanded operations at Solar Power Corp. By 1977, PV modules had

come down into the $20 / Wp range and total annual PV production

exceeded 500 kWp worldwide, which was heralded as a major milestone.

In 1978, we designed and fielded the world’s very first

utility-interactive PV system (outside the fence of the government

labs) -- a 5 kWp system here in Quincy, MA that was used to power

the pumps and controls of a 7,500 sq.ft. solar thermal system -- and

went on to design and constructed the world’s very first zero-net

energy, solar-powered, utility-interactive residence here in

Carlisle, MA in 1979. The rest, as they say, is history.

Julia Hamm

President & CEO

Solar

Electric Power Association

![]()

It's hard to believe that I've been involved with the solar industry

for 11 years now. What makes me a veteran in the solar realm still

leaves me as a newcomer to the larger electric industry. But in

those years, I've seen the U.S. solar market blossom and believe we

are just now on the verge of the true mainstreaming of PV.

When I first started working with electric utilities back in 1999,

the topic of solar almost never reached the executive level. Today,

many large utilities across the U.S. have a Vice President of

Renewables, and solar is an important part of their energy supply

strategy for the near- and long-term. Solar is now a frequent topic

of discussion in the utility boardroom and office of the CEO. PG&E,

a single utility, has already announced plans for more than 1.5 GW

of utility-side meter PV projects to come online between now and

2016. That does not take into account other future large-scale

project plans yet to be announced and the significant amount of PV

that will continue to be integrated into PG&E's grid by its

customers. Most exciting about what is now happening is that it's

no longer only California utilities that are recognizing the value

and importance of PV. Utilities from New York to Oregon to Hawaii

are preparing for PV to represent a significant portion of their

energy supply in the not-too-distant future. To successfully

integrate a high penetration of this intermittent resource will

require utilities to alter the status quo when it comes to business,

technical, and regulatory matters, but they are stepping up to the

plate to prepare for this challenge.

Historically in the U.S., the relationship between the utility and

solar industries has been an adversarial one, but today that is

changing. In order for PV to make a significant contribution to the

world's -- and the nation's -- CO2 reduction challenge, the actions

of homeowners and business owners alone installing rooftop solar

won't get us there fast enough. Utilities are the key to wide-scale

installation and integration of significant levels of solar

electricity on both the small-distributed-rooftop scale and the

large-central-station-power-plant scale.

Barry Cinnamon, CEO Akeena Solar

In 1985, according to Doc Brown in Back to the Future,

you needed a nuclear reactor to generate 1.21 gigawatts (pronounced

"jiggawatts").

So what's changed since then, or since 2001, when I got back into

solar?

1. Except for First Solar's success with thin film for large ground

mounts, the basic technology hasn't changed. Crystalline panels

were working in 1985, and are still working great now. It's an

evolution of technology, not a revolution. I expect forms of

crystalline panels to continue to dominate the market --

particularly for Distributed Generation.

2. Now that prices for panels have come down and are no longer the

biggest cost factor, increased attention is being paid to

installation costs. There are enormous improvements that can be

made in this area (such as our Westinghouse panels) -- and in the

amount of paperwork that is required. It's a hell of a lot easier

to save $0.20 per watt on installation/paperwork costs than to

reduce panel costs by the same amount.

3. In the words of George Westinghouse, AC is better than DC. To

keep the metaphor going, it's Back to the Future, with AC panels

becoming the dominant technology for rooftop solar -- for both cost

and safety reasons. No more High Voltage!

4. Incentives. I've never met an incentive I didn't like -- as long

as it got traction in the market. The Federal ITC and California

rebate programs are the two most successful incentives in the U.S.

Other states have tried programs, but their lack of consistency has

resulted in a damaging series of starts and stops. So far, here in

the U.S., we've been too chicken to establish a long term feed-in

tariff that will actually works. Germany did it, Ontario is doing

it -- but when we try, we set the FIT at a level that is either too

low to gain traction (like in California) or we create a program

that is hobbled by inadequate funds (e.g., Gainesville, Fla.).

5. Obviously, I'm a fan of branding -- especially when the

underlying product is a commodity. Just about anyone can make a

cheap, tasty soda, but unless it's called Coke or Pepsi, it's a

struggle to get people to buy it.

Ron Kenedi, Vice President

Sharp Solar Energy Solutions Group

![]()

Thirty years ago, the solar industry was a pre-niche market -- a

gleam in peoples’ eyes.

It was a market borne of absolute necessity, primarily for use in

remote areas or for the space program. There were experimenters and

folks who were working off-grid who wanted to use the technology.

And a few survivalists, as well -- solar was a technology that could

help them live remotely.

My first customers in solar were industries that needed solar for

remote applications like off-grid living and working. This included

ranching and industrial applications such as monitoring and

telemetry of oil platforms and gas flows; lighting, call boxes,

signage, water pumping, village power and water delivery. Solar was

also used in recreation, to help power RVs and boats. And today,

many of those original applications are still going strong.

Back then, we didn’t even contemplate the concept of 10 gigawatts.

Solar modules were 50 or fewer watts, and arrays were about 2 or 3

modules. Every thing was so much smaller.

Including the paychecks.

I remember when my business passed the $1 million mark.

Interestingly, a lot of those people who were working in the solar

business decades ago are still in the solar business. That’s a

credit not only to the technology, but to the commitment of the

people in this business. The original believers. People who were

drawn to solar because of their lifestyle and their system of

beliefs.

Everything was a lot smaller at the outset; there were very few

people were working in solar, and everyone knew each other. Today,

as opposed to the beginning, we have a gigantic industry with growth

that’s got no end in sight. We now have a lot of people in the

business who want to make their mark in this industry. People who

want to see science in action, further their careers -- and make

money.

The uses of solar are quickly evolving. We’re seeing tremendous

growth in grid applications. Solar is now powering homes and

businesses -- and now it’s providing technology for power plants.

Julia Curtis, Director, Business Strategy and Government Relations for Solar at BP

Solar needs to be more than a small but bright glimmer in our

energy mix. Milestones are important, and the U.S. is still behind

other countries for solar installations: the United States should

achieve 10 gigawatts of installed solar by 2015, and given the solar

resources and energy needs of the U.S., this is an achievable goal.

The U.S. solar market lacks the level of political consistency that

is necessary, and with the Treasury Grant Program set to expire at

the end of this year, there is a push to meet the start-construction

deadline of December 31, 2010. However, extending this deadline is

critical to reaching the 10 GW goal, and will help create jobs in

this rough economy. It is through one united voice that solar PV can

reach this goal, and begin to take on a significant portion of

America's growing energy demand. As with all energy sources,

government policy and incentives are critical to growing the market.

Solar energy clearly provides clean, reliable energy -- so why can't

we do a lot more?

Both China and India made headlines with solar projects in 2009,

including BP joint venture manufacturing plants to help expand their

solar power capacities to 20,000 megawatts by 2020. However, the

largest area of job creation in the energy sector is through the

installation of distributed generation solar. It will take policies

like net metering, interconnection standards, financing programs

like PACE and other state and federal clean energy leading programs,

and feed-in tariffs to meet this goal. We need bigger goals,and

long-term, consistent policies to help hedge against volatile and

increasing energy prices, creating more energy independence.

Paul Maycock, PV Energy Systems, solar pioneer with 40 years in the industry

In 1995, I forecast 8 to 10 megawatts in 2010 with an average price of $2.00 per watt. The sad part is that the world market is 90 percent subsidized, especially in Germany. The real milestone will be when we reach installed costs of $2.00 per watt. This will result in "grid parity," where PV with net metering is equal in cost to retail price in many of the markets of the world (though probably not in Germany). I forecast this will happen in 2015, especially by First Solar.

See Part 1 of this series here.