The 12-step Solar Program: Toward an Incentive-less Future

California, USA -- The un-incentivized future approaches, and it is time to call off the hunt for the next big incentive -- because if the solar industry (all technologies) does not, it is surely doomed. Well, maybe doomed is too harsh, disappointed is better. Along with disappointed add chronically over capacity and consistently margin constrained.

Extremely low prices for crystalline technology set expectations for even lower prices. Low prices in combination with generous FiTs stimulated demand at extraordinarily high levels. Demand boomed, and most FiT markets crashed. Here's the golden rule of incentives: they are expensive, and someone has to pay the bill.

Assuming a constant upward trend in solar demand is dangerous, even though historically the trend has always been up. As incentive rates decrease, eventually disappearing or transforming (yet again) altogether, demand will hinge on the industry's ability to lower installation costs (the module is a component of a system) while increasing technology efficiency and lowering manufacturing costs. System performance will become even more crucial, and investors will need to believe that the industry can thrive without incentives. Grid parity is a phrase tossed conveniently around at conferences when companies are seeking investment, and in marketing materials -- and considering the subsidies that conventional energy enjoys, it's unfair. But fairness does not matter. Solar is big business now: gigawatt-level, risky big business.

Memo to Good Analysts: Widgets Count

Now is the time when analysts look back and count widgets (cells and modules). 2010 looks to have been at least a 16GWp year, or 103% growth in vs. 2009. Figure 1 presents global industry growth (shipments to the first point of sale in the market) from 1995 through 2010. From 2005 through 2010, compound annual growth for the PV industry was 63%.

|

| Figure 1: PV industry growth, 1995-2010. |

Where the technology came from and where it ended up remains a tense issue for solar industry participants. As indicated in Figure 2, 56% of technology came from China and Taiwan (at least 37% from China), while ~81% went to Europe.

|

| Figure 2: Supply vs. demand, 2010. |

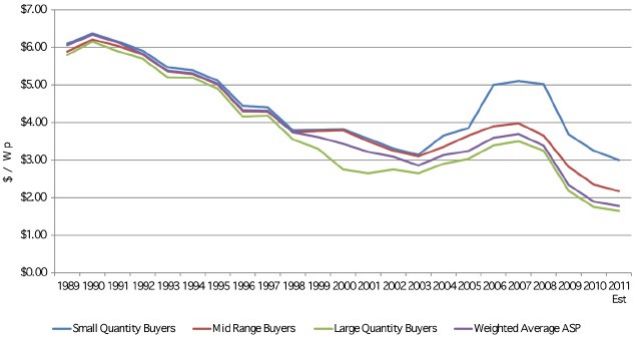

Back to the pesky issue of pricing. In 2009, technology prices (cells and modules) crashed after steadily increasing for several years. Those price increases came during the beginning of the FiT phase of PV industry history (2004-2008). But in 2009, manufacturers from China and Taiwan priced technology aggressively to gain share. The combination of low prices and generous FiTs stimulated escalating demand, and this expensive demand led to the current situation wherein markets need to be controlled. Figure 3 offers a view of average selling prices to the first point of sale, from 1989 through an estimate for 2011.

|

| Figure 3: Average selling prices, 1989-2011. |

A 12 step program for solar industry recovery from incentives

What the solar industry really needs is a recovery program, so that it can wholeheartedly approach a future in which incentives will likely not be generous -- if they exist at all -- and programs will be capped. After all, incentives were not meant to last forever (though those for conventional energy well may). The following twelve steps are meant to provoke thought and help an industry that has become addicted to incentives -- though realistically, these market stimulation tools are still necessary.

- Admit it -- the industry has become powerless over demand, and most markets have become unmanageable.

- Focus on lower technology and system costs. Develop innovative and standardized installation techniques. These may well wean the industry from a reliance on incentives.

- Focus on the system. Fit the technology to the region, the customer, and the application.

- Develop products -- not just technologies -- tailored to the application and the customer. BIPV is not just shingles or roof tiles.

- Look for three characteristics in markets and customers: a need for a reliable electricity source, price elasticity, and undaunted by the high upfront cost.

- Stop banging the grid parity gong. Talk about competitive electricity pricing market by market based on solar attributes.

- Delight the customer. That's just Marketing 101.

- Form a consortium among manufacturers to discuss how most FiT markets were destroyed, and how to avoid this in emerging markets such as the US, China and India. This is not collusion, it is common sense.

- Invest in system design and balance of systems. This is worth repeating -- it's not boring, and it is crucial to industry survival.

- Hey, governments: All solar is amazing. Stop looking for a magical, heretofore undiscovered magic technology or material that will change industry dynamics forever. All of this stuff sits in the sun for >25 years and reliably delivers electricity. What more do you want?

- Hey, governments and politicians: Progress isn't cheap. Renewable energy and solar is the future, and getting to it will be expensive. So was the Industrial Revolution, and going from wagon trains to railroads, and the Pony Express to the telegraph. Toilets were once options in houses, not mainstays. Stay committed. Develop controlled incentives -- the industry still needs them, and will have a difficult time without them.

- Hey, industry: FiTs are a-changin'. The trend is clear: FiTs as the industry has known them recently (and seriously, FiTs are a recent industry phenomenon) are changing. Adapting to this change is crucial. So, you'd better adapt.

![]() To subscribe or visit go to:

http://www.renewableenergyaccess.com

To subscribe or visit go to:

http://www.renewableenergyaccess.com