What's Driving North America's Solar PV Market in 2012?

February 7, 2012

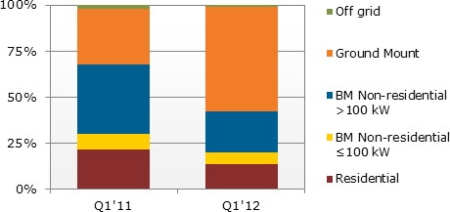

New Hampshire, U.S.A. -- The North American solar photovoltaic (PV) market tacked on nearly another full gigawatt (GW) of installations in 4Q11, echoing a late-year surge seen in other markets (think Germany and Asia), says NPD Solarbuzz. New Jersey, California, Arizona, and Ontario accounted for two-thirds of that demand; more than half (59 percent) was for large-scale ground-mount systems.

In the U.S. overall, thank the expiring US Federal Cash Grant for accelerating project activity to beat the year-end deadline. At the state level, California's Solar Initiative ratepayer program brought in an extra $200 million during the quarter, helping to pare down a long waitlist of customer-side distributed generation. Also, as part of California's Renewable Portfolio Standard target (33 percent of energy from renewable sources by 2020), the state is implementing several programs to stimulate distributed generation projects ranging form 1-20 MW.

In New Jersey, though, that 4Q11 growth might be short-lived, thanks to an oversupply of Solar Renewable Energy Credits (SRECs). Neither NJ nor Pennsylvania has adjusted their RPS solar obligations to fix an SRECs oversupply, says Solarbuzz.

Moving above the border to Canada, large-scale projects completed during 4Q11 were already approved under Ontario's previous incentive program, the Renewable Energy Standard Offer Program (RESOP). The feed-in tariff (FiT) program that replaced it spurred roughly 100 MW of smaller-scale residential and nonresidential projects in 2011, says Solarbuzz, while large-scale systems under the FiT have been slow to start due to regulatory and approval delays. Other areas such as project financing and product supply agreements are showing progress, though, suggesting projects are well advanced and should install in 2012.

(Note that solar PV industry watchers define "installations" differently, e.g. announced projects, shipped modules, actual grid-connection, etc. For its part, Solarbuzz calculates "installations" as modules that arrived at the end-site, not completion or interconnection. This is significant, because the timing between module shipments, installation completion, and grid connection can be months or even quarters. For what it's worth, Maxim's Aaron Chew calculated combined U.S. and Canada installs at 2.24 GW)

North American share by photovoltaic market segment. BM = building mounted. (Source: NPD Solarbuzz)

2012 Trends: Fragmenting US Markets, Canada's New FiT

Looking ahead into 2012, the U.S. has a 25 GW pipeline for nonresidential and utility solar projects, some of which qualified for the Cash Grant, meaning they can only ship and be installed this year, points out Solarbuzz senior analyst Junko Movellan. [Update 2/8: Movellan subsequently clarified this point: "Projects can be installed up to at the end of 2016 as long as project developers can either prove that physical work of a significant nature had begun by the end of 2011, or that the applicant paid or incurred 5.00% or more of the total cost of the specified energy property before the end of 2011."] And residential demand will grow only modestly in 2012, with lower system prices and lease financing programs mostly balanced by declining market prices in the five key states that have met their RPS requirements. Price reductions in 2011 were accelerated by Chinese module supplies; the U.S. vs. China solar trade dispute further reshaped supply and pricing toward year's end, and the official ruling for it (now due in late-March) "will shape the 2H12 supply mix," she notes.

And look for more restructuring in downstream channels as end markets shift. Larger downstream companies will run away from residential demand as it fragments into smaller state markets, while new project development entrants clamor to bring nonresidential and utility project pipelines to market, says Solarbuzz.

Canada's 2012 solar PV market will hinge greatly on the review of Ontario's FiT program that started in October, and whether key elements of the existing program structure are retained, notes Solarbuzz analyst Michael Barker. He anticipates rates falling between 10-30 percent, "in concert with greater specificity on technology or customer-type goals."

© Copyright 1999-2012 RenewableEnergyWorld.com - All rights reserved. http://www.renewableenergyworld.com