SoberLook Commentary: US Mortgage Refinancing Activity Going Strong - for Those Who are Eligible

Author: Walter Kurtz

As the US mortgage rates continue to decline to new record lows,

the refinancing activity for those who are eligible has been quite

robust. Just when borrowers sign the papers for a new mortgage

(particularly in situations when the bank covers the closing fees),

they are ready to refinance again. Some households have done this

more than once this year alone.

|

| Source: Bankrate.com |

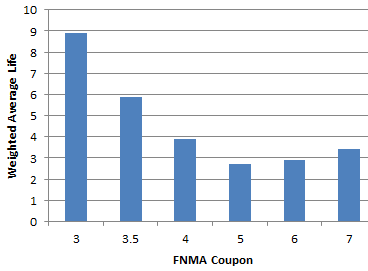

You can see the refinancing wave by just looking at the weighted

average life (WAL) of FNMA 30-year securities (Agency MBS). The

shorter the average life, the more refinancing is taking place (if

everybody in the pool refinances a year after getting

their mortgage, WAL would be one year). Here is what WAL looked like

in March for different coupon FNMA bonds.

|

| March 20th, 2012 |

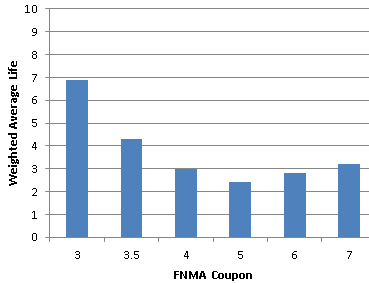

And here is what it looks like now. The 3% and the 3.5% coupon FNMA

securities (roughly corresponding to 3.6% - 4.1% mortgage rates) WAL

decreased by some 2 years in a short span of time. Note that the

high coupon securities represent mostly pools of borrowers (who

borrowed at higher rates some years back) that can't refinance

because their mortgages are "under water" (low to negative equity).

And the WAL declines in that part of the curve are barely visible.

|

| July 10th, 2012 |

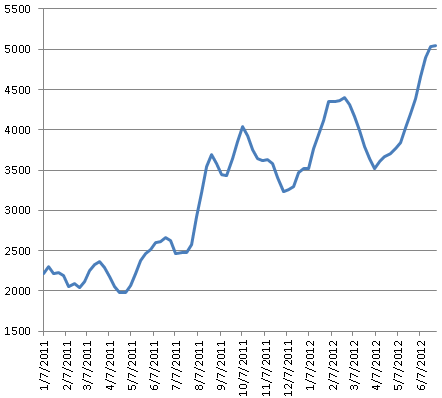

Mortgage applications for refinancing continue to stay strong as

well.

|

| Mortgage Applications for Refinancing - 4-week moving average |

So far all this refinancing has not translated into material

improvements in consumer spending, as savings from reduced mortgage

payments simply help households

further reduce leverage.

![]()

To subscribe or visit go to: http://www.riskcenter.com