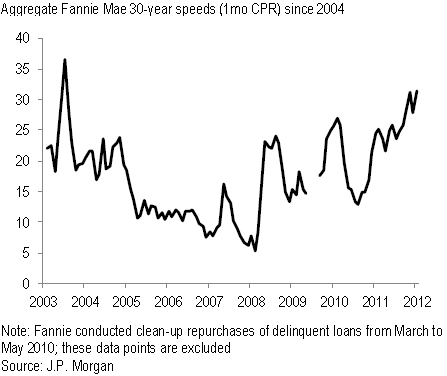

|

| Source: JPMorgan |

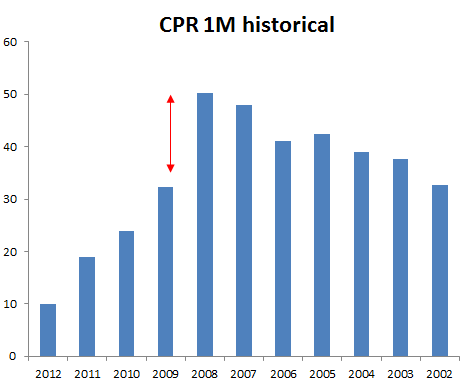

Most assume that this is all coming from recent mortgages with low loan-to-value ratios. As rates decline, those who took out a mortgage in 2010 for example are now refinancing it. But there is a bit more to the story. If one looks for example at the 5%, 30-year FNMA pool (these are loans paying roughly 5.5% interest on average), a different picture emerges. The pre-2009 "vintage" mortgage prepayment speed for these high coupon mortgages is higher. The chart below shows CPR (prepayment rate) by mortgage origination year.

|

| 5%, 30-year FNMA CPR (source: Credit Suisse) |

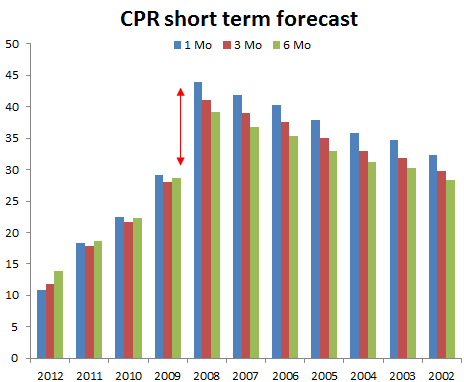

The short-term prepayment forecast from Credit Suisse looks similar. It means that the older mortgages with homes that are more likely to be "under water" are actually refinancing faster.

|

| 5%, 30-year FNMA CPR forecast (source: Credit Suisse) |

What's going on here? The answer has to do with the Home Affordable Refinance Program (HARP). It's a little venture run by the US Treasury and HUD. HARP was set up to help borrowers who are current on their payments but with homes that have dropped in value so much that it makes them ineligible for bank refinancing. The FHA has its own version of HARP as well. Here are the requirements (from HARP):

So that's how 2009 cutoff comes into the picture. Those who took out a 5.5% mortgage (for example) after 2009 and could refinance, already did - that's why the refi speed after 2009 for these mortgages is lower. But those in the pre-2009 bucket are refinancing via HARP. According to JPMorgan, under the second HARP program, a million borrowers have refinanced their mortgages in 10 months. The program is expected to be in place until the end of 2013. The combination of HARP and the Fed's MBS purchases keeping rates low, mortgage refinancing is expected to stay elevated next year. And of course mortgage originators should do quite well in this environment. In fact banks are boosting staff levels to deal with the refi wave.

- The mortgage must be owned or guaranteed by Freddie Mac or Fannie Mae.

- The mortgage must have been sold to Fannie Mae or Freddie Mac on or before May 31, 2009.

- The mortgage cannot have been refinanced under HARP previously unless it is a Fannie Mae loan that was refinanced under HARP from March-May, 2009.

- The current loan-to-value (LTV) ratio must be greater than 80% ["under water" mortgage ineligible for standard financing].

- The borrower must be current on the mortgage at the time of the refinance, with a good payment history in the past 12 months.

JPMorgan: - Sustained by HARP 2.0, and then QE3, [the refi wave] is poised to last well into 2013 and eclipse the prior record in duration, though not in magnitude. Extended periods of low rates compel originators to expand mortgage banking capacity to take advantage of the business opportunities.

|

| Source: JPMorgan |

![]()

To subscribe or visit go to: http://www.riskcenter.com