But what if a bank invests in a finance company whose primary business is lending to corporations. That should be permitted under the Volcker rule - at least based on the rationale behind the rule. But what if the finance company is a partnership that is structured like a private equity fund and its role is to lend to companies - as a bank would. Is that OK? And what if the fund makes risky corporate loans - possibly subordinated and unsecured high yielding loans. Is that "crossing the line"? The Volcker Rule does not prohibit a bank from making risky loans - in fact there is nothing in the Dodd-Frank legislation that prohibits banks from doing so. The US actually needs more risky business loans, not less, in order to get the economy moving. After all most small and midium-size business loans are risky by their nature. So why can't a bank jointly with investors own a company that makes such loans?

Such funds are actually quite common. Some are managed by private equity firms like KKR, while others are managed by banks like Goldman. In the case of Goldman (and other banks), the bank is also an investor in its own fund. From the investors' perspective that's a good practice to have the bank co-invest with them in order to eliminate potential conflicts - many investors in fact demand that banks invest alongside with them.

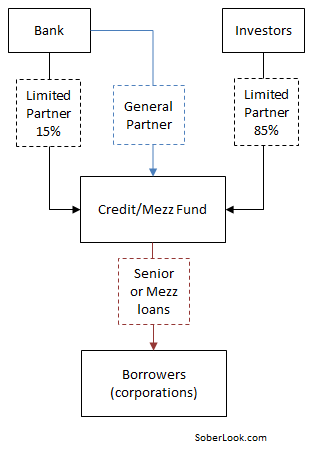

Some of these funds are called "mezzanine" ("mezz") funds because the loans they make tend to be in the part of the capital structure that is below the senior debt but above the equity. Goldman for example makes a great deal of money in this business as a GP (management/performance fees) and as an LP/investor (mostly income from these loans). The firm, together with other banks, has lobbied hard to allow it to stay in this business. Now the question before the regulators is whether such practices by banks should be prohibited.

WSJ: - Credit funds lend to companies that might not otherwise get financing, such as companies backed by private-equity firms, and tend to hold their investments to maturity while using a limited amount of leverage. Goldman has argued in meetings with regulators and in letters to them thatthese funds function like banks, just with a different structure, according to public records and the people familiar with the efforts.

The firm has argued that the funds help the economy by broadening the availability of credit and are less risky than other investments constrained by the Volcker rule. Regulators' response has been noncommittal, the people said.