|

| Source: Bloomberg |

That means QE3 purchases will not directly impact longer duration bonds (at least not as much as the 5yr notes). The longer term part of the curve will therefore be driven by inflation expectations. And longer term inflation expectations, as implied by the TIPS yields, rose sharply today.

|

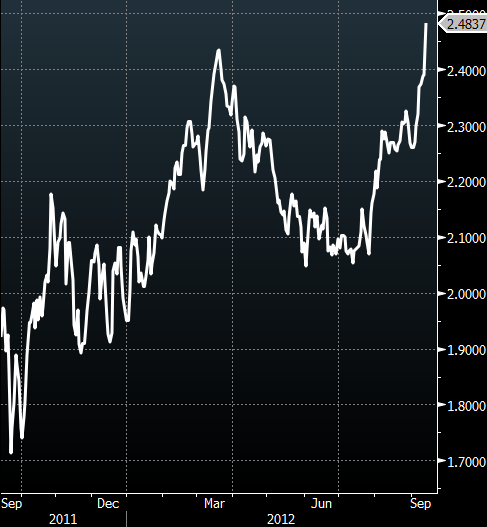

| 10y inflation expectations (10y breakeven) |

The combination of the Fed's expected shorter duration purchases and longer term inflation expectations forced the treasury yield curve to steepen. The market is beginning to price in rising inflation and there is only so much negative real yield investors will tolerate.

![]()

To subscribe or visit go to: http://www.riskcenter.com