Both show a recent "risk-on" spike. However, while the CS index is materially below its March-April peak, the Fisher-Gartman index is at the highest level since the index was launched.

|

| CS Risk Appetite Index (CS) |

|

| Fisher-Gartman Risk-On Index (CNBC) |

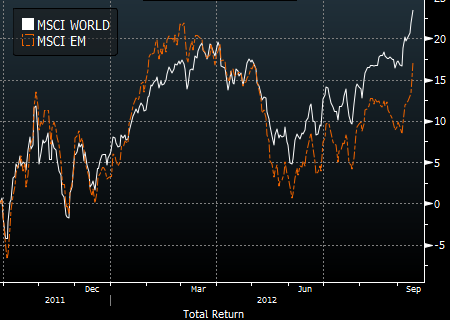

As discussed earlier, the CS index is sensitive to the global equity and credit markets, while commodities, currencies, as well as equities drive the Fisher-Gartman calculation. The main difference this time however came from emerging market equities, a larger component of the CS indicator than the Fisher-Gartman index. Emerging markets have underperformed the overall global equities index.

|

| MSCI World and MSCI EM total return (Bloomberg) |

Given these subtleties in the risk indicators related to emerging markets equities, let's take a look at a third measure, the Citi Macro Risk Index, to "break the tie". Here is the definition:

The Citi Macro Risk Index measures risk aversion in global financial markets. It is an equally weighted index of emerging market sovereign spreads, US credit spreads, US swap spreads and implied FX, equity and swap rate volatility. The index is expressed in a rolling historical percentile and ranges between 0 (low risk aversion) and 1 (high risk aversion).

This measure is based on credit spreads and implied

volatility indicators. Note that the index is inverted

relative to the two above, indicating the perceived level of

risk in the markets rather than the risk appetite.

|

| Citi Macro Risk Index (Bloomberg) |

Other than the underperformance of emerging markets equities, the overall risk aversion seems to be declining toward multi-year lows. Welcome to the new "new normal", where central banks set the level of risk appetite - and right now they simply want risk to be ignored.

![]()

To subscribe or visit go to: http://www.riskcenter.com