The FOMC is Running Out of Excuses to Maintain Current Policy

The retail sales measure from the Commerce Department survey came

in below expectations today with 0.2% month-over-month change vs.

0.3% expected. Given that the numbers missed the forecast, why then

did treasuries sell off sharply after the release?

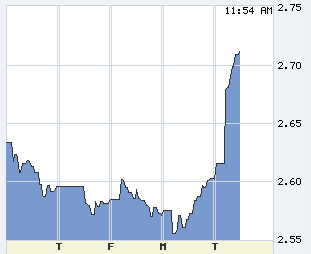

|

| 10y treasury yield (source: WSJ) |

The answer is that while retail sales growth has not been

spectacular, it is sufficiently strong for the Fed to begin reducing

its securities purchases shortly. Sales ex-autos were up 0.4% (auto

sales are volatile and other recent indicators of auto sales have

been strong.) The year-over-year ex-auto retail sales number is

historically on the lower end, but falls within the 2.5%-5% range

that some view as stable.

Given that the consumer is such a large part of the GDP, some

economists are already revising their GDP forecasts up. The FOMC now

has only one key potential showstopper: the ultra-low inflation rate

scenario. As James Bullard pointed out in his

June speech, inflation measures were collapsing earlier this

year (see

post), raising the specter of deflationary risks. If that trend

were to continue, the Fed would go into a holding pattern.

But inflation indicators in the US seem to have stabilized.

Commodity prices have bottomed out (for now), as copper bounced (see

post) and energy prices remain elevated.

|

| CRB BLS Spot Index of 23 commodity markets (source: CRB/barchart) |

Moreover, market-implied inflation expectations have risen since the

dip earlier this summer.

|

| 10 Year

TIPS/Treasury Breakeven Rate (implied inflation expectation; source: Ychart) |

With deflation no longer a high probability near-term threat, the

FOMC has run out of excuses. Unless the labor market suddenly takes

a material turn for the worse this month, we should see the

beginning of the end for QE3 shortly.

![]()

To subscribe or visit go to: http://www.riskcenter.com

http://riskcenter.com/articles/story/view_story?story=99915716