Once again some analysts in Europe

question the potency of the

so-called currency wars launched by

Japan and the US. The euro-yen

currency cross has had an

unprecedented rally, changing the

export landscape where Japan and

Europe (particularly Germany)

compete.

|

|

Yen per one euro (EUR/JPY) |

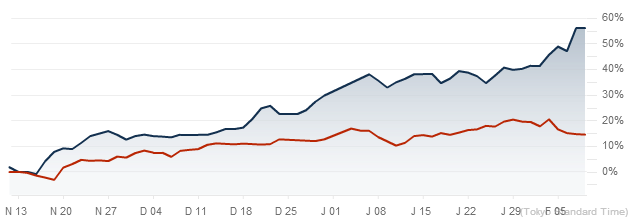

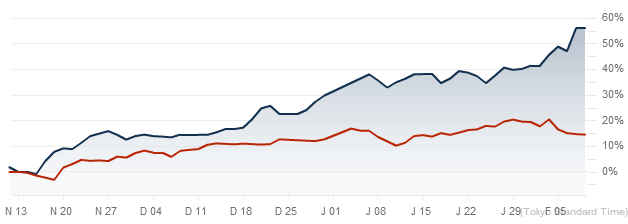

The impact of this adjustment in

currencies is quite visible in the

shares of exporters. The chart below

compares share prices of Volkswagen

and Toyota - as an example. It

demonstrates once again how

effective currency wars can be (

see

discussion). Weak yen is making

Japan's products cheaper and/or

margins higher.

|

|

Toyota (blue) vs. Volkswagen

(red) |

This trend is likely to negatively

impact the Eurozone's economy,

which, for the first time since the

start of the euro crisis, is

starting to show signs of recovery (

see

post). The question now is

whether the ECB is going to

"retaliate" in the currency war by

attempting to weaken the euro.

Bloomberg: - Since the

European Central Bank president

talked up the economic outlook

last month and signaled that the

worst of the debt crisis is

over, the euro has surged to a

14-month high against the

dollar. Banks have fueled the

euro’s rally by paying back more

emergency loans than forecast,

shrinking the ECB’s balance

sheet just as the Federal

Reserve and the Bank of Japan

expand theirs.

That’s threatening to stymie

Europe’s recovery before it has

begun, highlighting the

tightrope Draghi is walking as

he seeks to boost confidence

without encouraging euphoria.

With looser monetary policy in

the U.S. and Japan weakening the

dollar and the yen, the ECB may

soon come under pressure to

enter the so-called “currency

war” and rein in the euro,

economists said.

“The euro-zone economy needs

a rising euro like it needs a

hole in the head,” said Nick

Kounis, head of macro research

at ABN Amro in Amsterdam. “If

verbal intervention does not

stem the euro’s upward trend,

the central bank may eventually

once again consider rate cuts.”

So far however the ECB has stayed

away from direct asset purchases.

Bloomberg: - “A significant

shift is underway in global

central banking,” said Paul

Mortimer-Lee, global head of

market economics at BNP Paribas

SA in London. “There is a

worldwide currency war and the

ECB seems to be a central bank

that is not targeting the real

economy as much as the Fed, the

Bank of Japan and the Bank of

England,” he said. The ECB

“risks being the loser.”

It is expected that Draghi will

retain a highly dovish stance (as he

announced today) with respect to

the ECB's policy but will not

explicitly target a lower euro.

Barclays: - ... Draghi may

adopt a more dovish tone to

convince market participants

that monetary conditions will

remain loose, but we view any

specific ‘talking down’ of the

EUR as unlikely. Based on

the check-list of indicators

from the ECB’s January press

conference (CDS prices, stock

market indices, realised

volatility, capital inflows,

Target 2 imbalances, confidence

indices, current account

balances), market developments

are likely to be viewed as

broadly positive by the ECB more

than offsetting any negative

impact from EUR strength.

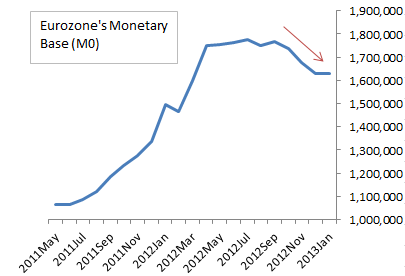

What makes Draghi's situation

particularly difficult is the fact

that the Eurozone banks have been

repaying some MRO and LTRO loans.

That is resulting in declines in the

EMU's monetary base (as bank excess

reserves drop). At the same time the

monetary base has been on the rise

in Japan, the US, and the UK. This

differential in base money growth

(h/t

Evil Speculator) continues to

pressure the euro higher (although

we are seeing a bit of a reversal

today). And European politicians as

well as some bureaucrats are

beginning to argue that something

should be done. For now, however, it

is expected that the Eurozone will

have to tolerate the relative euro

strength, as the ECB stays out of

the currency wars.

|

|

Source: ECB |

Econoday (today's ECB

announcement): - Perhaps more

significantly, Drahi's opening

remarks made no mention of the

exchange rate despite some

speculation that the central

bank might have become concerned

by the euro's recent

appreciation. However, in

response to questioning, he

commented that current levels of

both the nominal and real

effective exchange rates are

close to their long-run

averages. This may not be

what the ECB would prefer given

the weakness of Eurozone

domestic demand, but it also

suggests that for now at least,

the level of the single currency

is not a major factor in setting

monetary policy. In turn,

this may be seen by speculators

as a green flag to take the euro

still higher.

SoberLook.com

http://soberlook.com/2013/02/the-ecb-staying-out-of-currency-wars.html