WHEN KEN ALEXANDER started working at the J&L steel mill in

Aliquippa, Pennsylvania, in the 1970s, he was one of 17,000 workers.

But the workforce quickly declined as the American steel industry

withered in the face of cheaper foreign competition. In 1984 J&L

shut the mill. Four years ago another mill where Mr Alexander had

found a job, across the Ohio river in Ambridge, also stopped work

because of the recession. He was one of a skeleton staff of 20 kept

on as watchmen.

Derelict mills pepper the region, loose sidings flapping in the

frigid Appalachian wind. The once celebrated steel industry around

Pittsburgh (whose football team is called the Steelers) survived a

series of crises over the years, notes Mr Alexander, but was further

diminished by each of them—until now. These days the Ambridge mill,

bought by a Russian conglomerate five years ago, is humming away.

Its 400 workers transform solid steel bars produced at another mill

nearby into seamless pipes, in demand by oil drillers, among others.

The management is taking advantage of a seasonal lull in demand to

straighten out kinks in the line and thus increase its capacity.

Other firms are making much bigger bets on the local steel

industry. Fifty miles to the north-west, in Youngstown, Ohio, a

French firm, Vallourec, has spent $650m building an entirely new

mill to make similar pipes. It began production in October, with

a staff of 350. Thirty miles in the opposite direction, in

Brackenridge, Pennsylvania, Allegheny Technologies is spending

$1.1 billion on a new mill to produce stainless steel and other

specialty metals. US Steel opened a new $100m mill in Ohio in

2011, also to supply the oil and gas industry. Timken, another

steelmaker, is spending $200m on its mill in Canton, Ohio.

The main reason for this flurry of investment lies a few

thousand feet below the ground: the Marcellus shale, a

geological formation containing huge reserves of natural gas

trapped in tiny pores in the rock. It is thought to be America’s

biggest gas field, stretching 600 miles along the Appalachians,

from New York to West Virginia., but has only recently begun to

be tapped, thanks to fracking and directional drilling.

Last year the government of Pennsylvania alone issued permits

for 2,484 such “unconventional” wells; 1,365 of them were

actually drilled. Wells in the Pennsylvanian part of the

Marcellus produced 895 billion cubic feet (bcf) of gas in the

first half of 2012, up from 435bcf in the same period in 2011

and almost nothing as recently as 2008.

Well lubricated

Driving through the south-western corner of the state, the

benefits of this “shale gale” are easy to see. New roofs,

fences, barns and tractors have sprouted on many local farms;

plenty of shiny new pick-up trucks ply the roads. By one

estimate, Pennsylvanians who allow drilling on their land earned

some $1.2 billion in royalties last year. Suburban office parks

are proliferating outside Pittsburgh, the biggest city in the

area, with space being snapped up by oil firms, their suppliers

and subcontractors, lawyers and environmental consultants. Even

the most basic restaurants are overflowing at lunchtime, a local

complains.

All told, the Marcellus already supports over 100,000 jobs in

Pennsylvania, according to an analysis by IHS, a research firm.

That figure is expected to rise to over 220,000 in 2020. Shale

gas gave the local economy a $14 billion boost last year, IHS

reckons, and will buoy it by almost $27 billion in 2020. All the

extra economic activity generated nearly $3 billion in taxes, it

calculates. A new “fee” (the Republican word for tax) on gas

production adopted by the state legislature last year should

help raise yet more in future.

Pennsylvania is just one of several states enjoying a

shale-gas boom. Arkansas, Louisiana, Oklahoma and Texas have all

seen similar rushes. Shale-gas production in the United States

as a whole rose more than fourfold between 2007 and 2010, says

the Department of Energy. That has helped push up its gas output

by 20% over the past five years, making the country the world’s

biggest gas producer. BP, a big oil and gas firm, forecasts that

North American shale-gas output, largely from the United States,

will grow by an average of 5.3% a year until 2030.

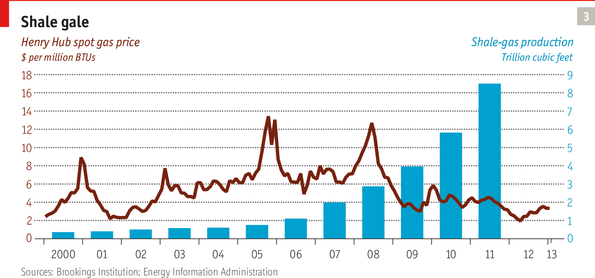

America is already producing so much shale gas that local gas

prices have plummeted, from over $13 per million British thermal

units (mmBTU) in 2008 to $1-2 last year. They have since

recovered slightly (see chart 3), but America still enjoys

remarkably cheap gas by international standards. In 2011 it had

the second-lowest gas prices for industry among rich countries,

after Canada, according to the International Energy Agency

(IEA). American factories paid a third of the German gas price

and a quarter of the South Korean one, the agency reckons—and

prices have fallen further since.

Cheap gas is also translating into cheap electricity, since

America’s marginal power supplies tend to come from gas-fired

plants. In 2011, according to the IEA, American factories paid

roughly half the going rate for electricity in Chile or Mexico

and a quarter of the eye-watering Italian price. In New York

last year prices were the lowest they have ever been since the

state introduced a competitive wholesale market in 1999.

Investors, naturally enough, are keen to take advantage of

such bargain prices. They have been pouring money not only into

steelmaking but all manner of energy-intensive industries, from

plastics to fertilisers. Just up the Ohio from Ambridge, Shell

is contemplating building a multi-billion-dollar “cracker” to

turn the ethane that emerges with much of the gas from the

Marcellus into ethylene, a feedstock for plastics.

On the Gulf coast (another gas hub), Chevron Phillips, Dow

Chemical, Formosa Plastics, Occidental Petroleum and Williams

are all expanding existing chemical plants or building new ones.

A chemical firm called Methanex is dismantling one of its

factories in Chile and shipping it to Louisiana to take

advantage of low gas prices. CF Industries is expanding its

local fertiliser production. Nucor, a steel firm, is building a

new mill. Sasol of South Africa hopes to build a refinery in

Louisiana to turn gas into petrol. Several firms want to

construct facilities in the region to liquefy gas and export

it—a dramatic reversal from a few years ago, when the need was

thought to be for import terminals.

America’s big pipeline network creates a relatively liquid

and fungible national market for gas, so customers far from any

shale beds are still able to take advantage of low gas and

chemicals prices. Orascom, an Egyptian conglomerate, plans to

build a $1.4 billion fertiliser factory in Iowa. Bridgestone,

Continental and Michelin are all planning to make more tyres in

South Carolina, reversing a long decline.

Better still, the steep drop in the price of natural gas has

driven America’s drillers to hunt for oil instead. Rigs are

migrating from gassy places like the Haynesville Shale, in

Louisiana, to spots where oil is trapped in tiny rock pores,

such as the Permian Basin and Eagle Ford Shale in Texas, the

Bakken formation of North Dakota and the Mississippian Lime,

which sits astride the border between Oklahoma and Kansas.

Applying the same techniques to such “tight oil” as to gas-laden

shales, they have managed to increase America’s oil production

by a third over the past four years, to 7m b/d. The government

expects it to grow by more than 1m b/d over the next two years.

The output of the Bakken Shale alone has risen from 100,000 b/d

in 2008 to over 700,000 now. By the end of this year, BP

predicts, America will overtake Russia and Saudi Arabia to

become the world’s biggest producer of liquid fuel, meaning oil

and biofuels.

The newfound oil brings just as much of a bonanza to the

places where it is extracted as the shale gas does. Flights to

previously obscure airports in North Dakota—Dickinson, Minot and

Williston—are full, as are all hotels within striking distance

of the Bakken. Property prices have shot up. The oil industry

now accounts for 15% of the local economy, according to IHS, and

has brought 72,000 jobs to a state with fewer than 700,000

people.

Despite its huge local impact, America’s shale-oil boom has

pushed up global oil production by just a percentage point or

two, not enough to reduce the price much. However, it has

resulted in a big drop in America’s import bill. IHS calculates

that unconventional oil reduced the trade deficit in 2012 by $70

billion, or about 10%.

All told, says IHS, unconventional oil and gas accounted for

$238 billion in economic activity, 1.7m jobs and $62 billion in

taxes in 2012. That includes the exploration and extraction

itself, the supply chains they rely on and the extra spending by

all those newly employed oilmen. But it leaves out the

second-order effects of cheaper gas, electricity and chemicals.

Last year the American Chemistry Council, an industry group,

forecast that over the next couple of years cheap gas would spur

some $72 billion in new investments in eight gas-hungry

industries alone. That, in turn, would lead to a further $342

billion in new economic activity in 2015-20, along with the

creation of 1.2m new jobs. The different levels of government,

for their part, would rake in an extra $26 billion a year in new

taxes.

An outsized bonus

In principle, all American companies and consumers benefit

from lower energy prices. The effect may not always be big

enough to spur heavy new investment, but it might be sufficient

to keep American factories with high labour costs going in the

face of foreign competition.

Economists at Citigroup and UBS predict that the shale gale

will lift America’s GDP growth by half a percentage point a year

for the next few years. Indeed, cheap energy is cited as one

factor by those who predict a manufacturing renaissance in

America. Labour in China is getting more expensive, the argument

runs, and so is shipping Chinese-made goods across the Pacific.

At the same time ever shorter product cycles confer an advantage

on factories located close to the people who consume their

goods. Quality is easier to maintain and intellectual property

easier to protect if the head office is not far away. Throw in

lower bills for power or petrochemicals, and bringing work back

home begins to look attractive.

For the moment America’s manufacturing output remains below

its 2007 level, and its trade deficit with China is still

growing. But some high-profile examples have caught the

headlines. GE has moved the production of some white goods from

China and Mexico to Kentucky, and Lenovo, the Chinese firm that

bought IBM’s personal-computer business, plans to return some

manufacturing to North Carolina. In the long run, however,

America will not be able to lure and retain investors like these

without a better-educated workforce.

Correction: The original version of this

article stated that the steel mill in Ambridge was bought by a

Russian conglomerate six years ago. In fact, it was five. This

was corrected on March 21st 2013.