More Polysilicon Plants Still Under Construction Despite Enormous PV Overcapacity – Why?

March 5, 2013

Contradictory trends are currently pushing the polysilicon industry to simultaneously restrict production volumes while continuing to add new capacity.

The rationale for reducing plant utilization is obvious. Between 2008 and 2012, with production levels substantially higher than demand, polysilicon prices have fallen at an average annual rate of 38 percent per year. In 2012 alone, prices fell 53 percent. As average polysilicon prices fell well below $20/Kg, well below cash costs for most makers, reducing utilization has been is the only way to stem loses.

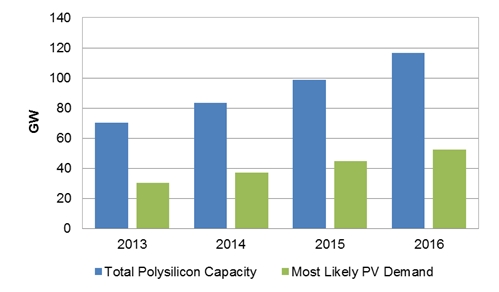

Despite there being available capacity well above that required by the PV and semiconductor industries, new (large) polysilicon plants are expected to come on line over the next several years. Based on new research featured in the NPD Solarbuzz Marketbuzz 2013 Report, polysilicon capacity is forecast to exceed the most likely PV demand by more than 100 percent for the next few years.

Forecast Polysilicon Capacity versus PV Market Demand

Source: NPD Solarbuzz Marketbuzz 2013 Report

This gap seems to defy logic. So what is motivating leading polysilicon manufacturers such as Wacker, Hemlock, Tokuyama, OCI, LDK, Daqo, Samsung Fine Chemical, Hanwha, Renesola and others to add yet more polysilicon capacity?

The reasons vary by manufacturer and investment phase:

- Some manufacturers are increasing capacity simply by “debottlenecking” plants or implementing new manufacturing technologies, such as hydrochlorination, to optimize their process and maximize output. (Debottlenecking typically increases productivity and lowers costs.)

- Other manufacturers are building new polysilicon plants as part of vertical integration strategies. Their goal is to lower downstream silicon costs by bringing an increased percentage of polysilicon requirements in-house.

- But the main reason the polysilicon capacity pipeline is still backed up is the long lead time to build plants, and the difficultly in stopping investments previously committed to. Polysilicon still seemed like a good bet when many of these projects were started. It may take 2-3 years (or even longer) from the time that a polysilicon plant is launched until it is able to start mass production. Indeed, once land is purchased, site construction commenced, and equipment ordered and delivered, it may be both politically and financially difficult to abandon a project.

It is unclear if (and when) all of this new polysilicon capacity will be ramped up. Wacker and Tokuyama, for example, have already stated they will complete current projects but will delay ramp up until market conditions warrant. And it is very likely that much of the Tier 3 (and even Tier 2 capacity) will be permanently shuttered over the next couple years.

At some point in the future, demand will finally catch up to supply. But unless demand grows faster than currently forecast, either more companies will exit polysilicon production or average plant utilization rates will remain depressed; and the gap between capacity and demand may continue to hinder many polysilicon makers’ ability to return to profitability for several more years.

This article was originally published on the Solarbuzz blog and was republished with permission.

![]() © Copyright 1999-2013 RenewableEnergyWorld.com - All rights reserved.

http://www.renewableenergyworld.com

© Copyright 1999-2013 RenewableEnergyWorld.com - All rights reserved.

http://www.renewableenergyworld.com