|

| Source: FocusEconomics |

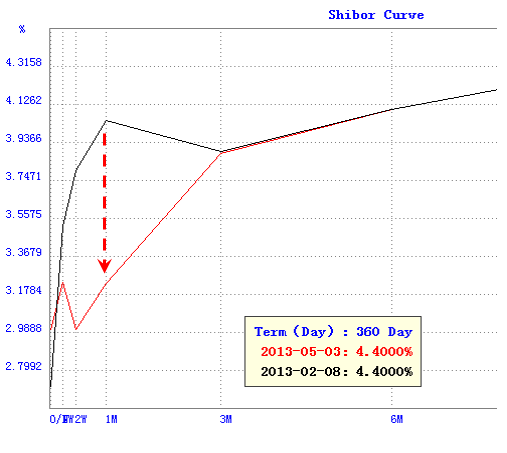

The increased liquidity is now visible in China's money markets, with short-term interbank rates declining in recent months.

|

| Source: SHIBOR |

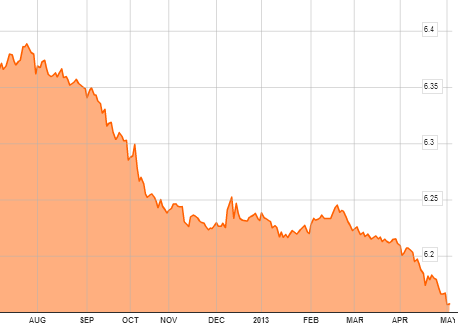

Capital is also pouring in from abroad as investors attempt to escape the zero-rate environments many developed nations are facing. The demand for yuan has been quite strong, driving CNY to new record highs.

|

| CNY per one dollar - spot rare (chart shows CNY appreciating/dollar depreciating; source: Bloomberg) |

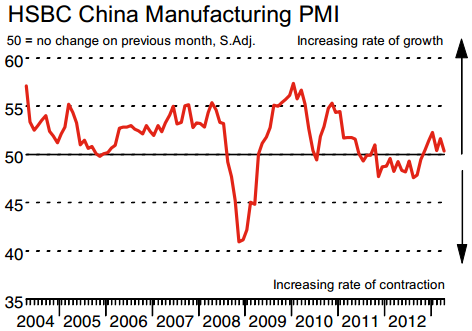

In the past, improved credit/liquidity conditions would result in stronger economic activity, particularly in manufacturing. That's no longer the case.

|

| Source: HSBC/Markit |

It seems that China has caught a developed nations' disease in which stimulus no longer translates into improved growth. As was the case in the Eurozone, China is suffering from what economists call "weak monetary transmission", a condition in which credit/liquidity is not getting to the areas of the economy where it's most needed (and in some cases there is simply no demand for credit).

DB: - The divergence between hard economic data and the enormous expansion of liquidity since the beginning of the year suggests that credit transmission mechanisms have broken down and the chances of a credit crunch are growing.

DB calls this the "law of diminishing returns" - more credit

doesn't mean stronger growth:

|

|

| Source: DB |

All this liquidity (which started last year - see post) may have avoided a "hard landing", but the bet on China's stimulus nurturing a renewed growth spurt has not worked out so far.

![]()

To subscribe or visit go to: http://www.riskcenter.com

http://riskcenter.com/articles/story/view_story?story=99915333