Bernanke: - We’re trying to make an assessment of whether or not we have seen real and sustainable progress in the labor market outlook. If we see continued improvement and we have confidence that that is going to be sustained, then we could in -- in the next few meetings -- we could take a step down in our pace of purchases.

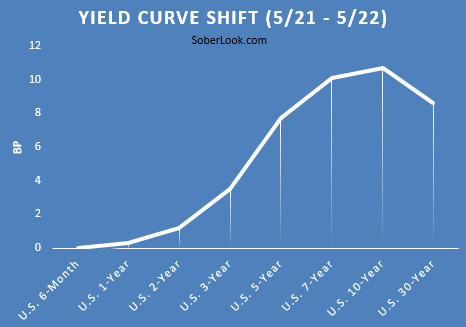

US equity and fixed income markets declined sharply in

response. To understand just how much asset prices depend on

this stimulus from the Fed, consider the move across the

treasury curve today. The increase in the 10yr yield was

larger than in the 30yr. The Fed does not hold much in the

long bond type durations relative to those that are 10yr and

shorter. The long bond is therefore not as exposed to the

Fed slowing its purchases as the 7-10yr notes.

The central bank's balance sheet - not the fundamentals - has been driving bond pricing and is the key determinant of the treasury curve's shape. Today was just a hint of how the eventual exit from QE may ultimately play out. This does not bode well for other asset classes (such as high-dividend shares which sold off sharply) whose valuations have become dependent on this stimulus rather on fundamentals.

![]()

To subscribe or visit go to: http://www.riskcenter.com

http://riskcenter.com/articles/story/view_story?story=99915402