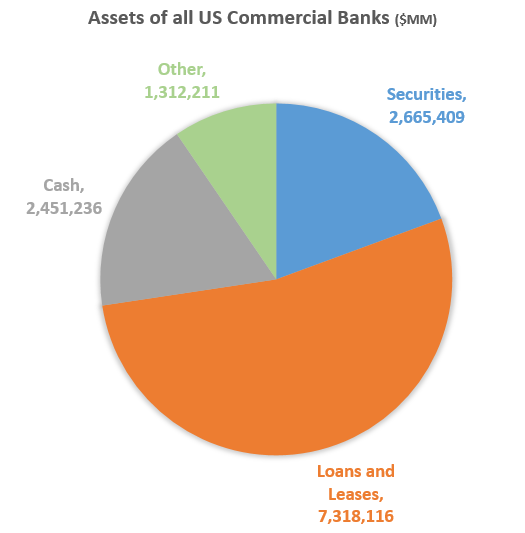

The first part of the answer is that loans and leases

represent just over half of banks' total assets in the US.

That's very different from many smaller countries where

lending may be a much bigger percentage of banks' holdings.

A US bank for example could provide financing in the form of

a registered bond (financing for a municipality or a

corporation), which would not show up in the loan-to-deposit

ratio.

|

| Source: FRB |

But the biggest problem with the "loans=deposits" school of thought is the assumption that banks operate in a static monetary base environment. This assumes that banks in effect are the only lenders. But these days the Fed is the largest single lender in the US and that's where a large portion of the deposit growth is coming from. The Fed is lending to the federal government and to the GSEs, which generates deposits at commercial banks. Every dollar the Fed uses to buy securities outright ends up as a deposit at some bank(s). As the chart below shows, this is one of the situations that increases deposits without any corresponding loan growth at commercial banks.

Through this process QE floods the banking system with deposits in hopes that all this liquidity (excess reserves) will spur banks to increase lending. However, for a number of reasons - some having to do with low demand for credit - that approach has not worked out as "planned".

![]()

To subscribe or visit go to: http://www.riskcenter.com

http://riskcenter.com/articles/story/view_story?story=99915932