Global Economic Outlook, April 2014

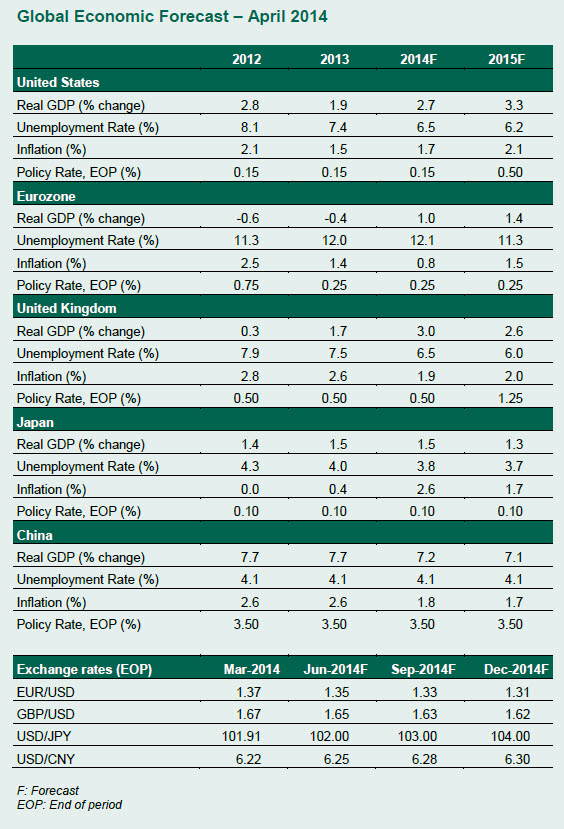

UNITED STATES

The fundamentals of the U.S. economy suggest a strong

performance in the rest of the year after a weather-related

setback in the first quarter. The absence of a drag from

cutbacks in federal government spending adds to the optimism.

The Fed will complete its asset purchases by year-end, with

labor market and inflation developments driving the timing of

any tightening. A likely increase in the labor force

participation rate should result in a measured decline of the

unemployment rate. The current subdued trend of inflation is

predicted to approach the Fed’s target of 2% as economic

momentum gathers steam. The dollar’s relative position is

expected to strengthen in light of the projected growth. The

shaky status of economic conditions in Europe and China are a

risk to the outlook of the U.S. economy.

EUROZONE

The Eurozone as a whole continues to edge toward recovery, but

the pace of growth remains very uneven across the region.

Germany’s real GDP growth will likely reach 2% or more this

year, up from 0.5% in 2013, but growth in France will likely be

no more than 0.5% in 2014 after a nearly steady reading in 2013,

and Italy is expected to remain mired in recession. Spain’s

headline growth of around 0.8% will not do much to diminish

unemployment that remains higher than 20% and a youth jobless

rate around 50% – levels that risk deep social dislocation and a

“lost” generation of young workers.

Inflation will remain very subdued across Europe, burdening the

European Central Bank (ECB) with a considerable policy dilemma.

It is not clear that cutting the refi rate even lower than the

current 0.25% will do much to stimulate credit growth. Eurozone

banks are focused on boosting their capital accounts as the

ECB’s first asset quality review and stress test gets underway.

Further, businesses and households alike are still deleveraging.

Some form of quantitative easing could kick-start moribund

economies, but crafting such a program across 18 separate

countries with diverse asset markets and differing macroeconomic

priorities would take time. High rates of unemployment will

continue to be a challenge, with the rate for the Eurozone as a

whole remaining just above 12% through 2014.

Sovereign debt yields in “peripheral” economies have fallen back

to levels last seen in 2007, but there is a perennial risk that

renewed debate over an issue such as Greek debt sustainability,

political turmoil in Italy or French policy clashes could

trigger another round of market volatility.

UNITED KINGDOM

Economic recovery continues in the United Kingdom, with real GDP

growth headed toward 3% this year. Inflation continues to abate

and should be just below 2% by the end of the year. The Bank of

England (BoE) has modified its forward guidance policy to

include a range of indicators, not just the unemployment rate,

but continues to signal that policy rates are unlikely to

increase until the first half of next year (and then only

gradually). Signs that the housing market recovery has spread

outward from London has raised concern that another housing

bubble could be in the making. The BoE’s Monetary Policy

Committee will not hike interest rates to curb house prices, but

its Financial Policy Committee (formed last year) is likely to

toughen up affordability tests and to look into other options to

take the froth out of the market.

JAPAN

Economic performance in the second quarter is expected to be

dismal, as consumers adjust to the 3% VAT increase that took

effect at the beginning of April. However, the economy is

expected to get back on track in the third quarter as consumer

sentiment improves and spending increases. Private consumption

is vital for the fledgling recovery as government stimulus

begins to taper off and export growth continues to disappoint.

While the government could add more fiscal stimulus in the

second half of the year or delay the planned 2% VAT increase

next year, the prospects for export-led growth are murkier as

continued soft demand in the United States and European Union

and a weakening Chinese economy combine to pressure exporters.

Real GDP is forecast to expand 1.5% in 2014 as fiscal stimulus

offsets weaker consumer spending due to the consumption tax

hike.

The Bank of Japan (BOJ) will likely maintain the current 0.1%

target policy rate while adding to its massive quantitative

easing program this summer to foster economic activity. After

missing last year, the BOJ is expected to reach its 2% inflation

goal this year as the consumption tax increase push prices up by

2.1%. Meanwhile, the yen is expected to continue weakening

moderately to 104¥/US$ by the end of 2014 while unemployment

remains benign at 3.8%. Risks to Japan’s outlook include the

collapse of Chinese import demand, a sustained decline in

domestic consumer demand and a loss in patience with Abenomics

and the absence of blockbuster announcements regarding the

structural reform arrow.

CHINA

China’s economy expanded at an annualized pace of 7.4%

in the first quarter, below the official 2014 target of 7.5%,

and the government renewed its claim that GDP growth was not as

important as the current job creation target. Beijing has

implemented a series of short-term measures to shore up the

economy, the most notable and controversial being an expansion

of the currency trading band in March, which was followed

immediately by the yuan falling about 3%. While the government

has not spoken about currency competitiveness directly, this

move provided a boost to exporters struggling in the first

months of 2014.

Inflation is slowing on the year, suggesting only weak price

pressures at best from the domestic economy. The government has

dismissed talk of fiscal stimulus, though public spending

measures designated for 2014 have been fast-tracked. There is a

significant concern that slowing growth and rising credit

figures are creating an imbalance that cannot be easily

reconciled without a sharp shock to the economy. GDP growth

appears set to remain just below the official target level this

year, though investment spending will remain at a worrisome

level. If economic growth continues to be bolstered primarily by

excessive and potentially unproductive lending, the excess

capacity and overvalued assets created will only expedite a

painful rebalancing.

The opinions expressed herein are those of the author and do not necessarily represent the views of The Northern Trust Company. The Northern Trust Company does not warrant the accuracy or completeness of information contained herein, such information is subject to change and is not intended to influence your investment decisions.

![]()

To subscribe or visit go to: http://www.riskcenter.com

http://riskcenter.com/articles/story/view_story?story=99916590