New Drilling Largely Driven By Debt

Major oil and gas companies are taking on an increasing share of debt in order to maintain drilling momentum, according to data from the U.S. Energy Information Administration.

Beginning around 2010, energy companies have been increasing their spending, particularly in the United States, as the tight oil revolution took off. Major firms snatched up acreage in oil-rich shale formations like the Bakken and the Eagle Ford and began drilling at a frenzied pace.

The significant outlays required to ramp up such an operation were offset by the rising price of oil, which allowed oil companies to expand their operations without having to take on substantial volumes of debt.

But after several years of increases, global oil prices began to plateau in mid-2011 and have stayed relatively steady since then. In fact, 2013 experienced the least oil price volatility since 2006.

And oil prices in 2014 have remained remarkably consistent, especially taking into account record levels of global demand and the abundance of geopolitical tension around the globe, from Ukraine to Iraq and Syria.

As a result of oil prices trading in a narrow band – roughly between $100 and $120 for Brent Crude and $90 and $105 for WTI – revenues for oil and gas companies flattened out even as their costs continued to rise.

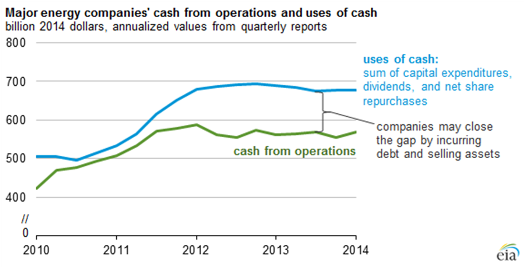

From 2012 through the beginning of 2014, average cash from drilling operations increased by $59 billion over the same average seen in 2010-2011. But spending rose at a faster clip: up more than $136 billion. The yawning gap that opened up between spending and revenues has largely been closed by the acquisition of more debt.

For shale drillers in particular, debt has doubled over the last four years while revenues grew at a meager 5.6 percent.

As the EIA points out, taking on debt is not necessarily a bad thing, especially if it is used to invest in new sources of production and growth.

But a new report from Taxpayers for Common Sense points to one other factor that may be contributing to the rise in spending long after earnings flat-line.

Under the U.S. tax code, oil and gas companies can defer billions of dollars in taxes by maintaining elevated levels of spending. That is partly by design. Drilling new oil and gas wells is capital intensive, and thanks to a provision in the 2009 stimulus bill, energy companies can use what is known as “bonus depreciation” to write off all depreciation in a single year, as opposed to spreading it out over future tax cycles.

The intended effect was to incentivize spending – to allow companies to earn immediate cash from producing wells and use that revenue to drill subsequent wells. Meanwhile, the country’s energy production receives a boost.

But Taxpayers for Common Sense sees something more nefarious. True, the companies theoretically have to eventually pay those tax bills, but in reality, the group argues, the tax incentives amount to a huge subsidy. By taking all the tax benefits upfront, energy companies don’t have to pay interest on billions of dollars in taxes that are pushed off to some point in the future.

“Often, in their financial statements, these companies tout how they finance their exploration and development investments with cash flow from operations. Yet, many have significant deferred tax liabilities. In effect, these companies are financing significant parts of their business with interest-free loans from U.S. taxpayers [emphasis in the original],” the report says.

Through the various peculiarities of the tax code, oil and gas companies already pay a much lower effective tax rate than the statutory 35 percent. ExxonMobil for example, paid a 19.3 percent effective tax rate between 2009 and 2013. But by deferring taxes, oil and gas companies can wind up paying even less than that.

But the heady days of drilling might be drawing to a close. The bonus depreciation allowance expired at the end of 2013 (although Congress is considering partially reinstating it). And although taxes can be deferred, energy companies will have to eventually pay their bill.

Also, much of the debt-fueled spending has been built on the back of low interest rates. With the economy improving, the Federal Reserve will soon end its program of extraordinary asset purchases, perhaps leading to a period of higher interest rates. This could dramatically raise the cost of drilling.

But more importantly, when oil and gas production stops rising,

heavily indebted energy companies could face a day of reckoning.

Oilprice.com

![]()

To subscribe or visit go to: http://www.riskcenter.com

http://riskcenter.com/articles/story/view_story?story=99916944