Energy storage compared to 2005 solar market

The next six years will begin to see long-term growth for commercial energy storage, according to GTM Research, driven in part by the growth of solar photovoltaics.

|

|

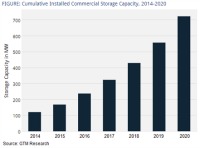

Click on image to enlarge. Credit: GTM Research |

The U.S. installs a solar system every four minutes, according to GTM, which creates widespread opportunity for the deployment of distributed energy. More than 720 MW of distributed energy storage will be deployed in the U.S. between 2014 and 2020, GTM forecasts, representing a 34 percent cumulative annual growth rate.

Energy storage can fulfill the roles of conventional generation, transmission, and distributed assets, as well as provide value in behind-the-meter applications. From a technical perspective, storage can be used to smooth the output and variability of solar energy and may ultimately lead to solar receiving larger capacity credits or help to avoid capacity charges.

However, the high cost of energy storage technologies compared to traditional grid alternatives has been a barrier to widespread adoption. Fortunately, that is changing with advances in battery technologies, cost reductions driven by mass production of batteries for consumer electronics and electric vehicle applications, and continuous improvements in balance of system costs for grid-integrated systems.

Other growth drivers for distributed energy storage include demand charge reduction for commercial and industrial customers, frequency regulation, and state-level incentives. California and New York have been the clear leaders in advancing storage initiatives, particularly for behind-the-meter assets.

"The commercial energy storage market is still in its earliest days, but we're starting to see real opportunity emerge for companies that can selectively pursue attractive markets and successfully monetize multiple value streams," said Shayle Kann, senior vice president of GTM Research.

GTM Research compares the current commercial energy storage market to the U.S. solar market of 2005. The technology, though still expensive, is sophisticated enough to allow for widespread adoption, and the business models are just beginning to emerge. A few geographies, driven by policy and incentive, will dominate distributed generation storage in the coming years.

Navigant Research is predicting that the rapid expansion of the microgrid market over the next 10 years is expected to bring with it increased demand for energy storage, which delivers services to microgrids similar to the services that energy storage systems delivers to the traditional grid -- resource optimization (fuel, solar photovoltaic, wind), resource integration (photovoltaic, wind), stability (frequency, voltage), and load management.

The total worldwide capacity of energy storage systems for microgrids will grow from 817 MWh in 2014 to 15,182 MWh by 2024, Navigant forecasts, with advanced batteries and, in some cases, flywheels taking progressively more market share from traditional lead-acid batteries as microgrid systems become more sophisticated.

"The primary value proposition of energy storage in a microgrid is in improving the payback period of the system, either by enabling an increase in the penetration of renewable energy sources, allowing participation in deregulated ancillary service markets, or reducing diesel fuel consumption," said Anissa Dehamna, senior research analyst with Navigant Research. "High prices for diesel fuel, a stronger push for the utilization of renewable resources in microgrids, and ancillary service market reforms will all underscore the business case for energy storage for microgrids."

For more:

- see this

report

© 2014 FierceMarkets. All rights reserved. http://www.fierceenergy.com

http://www.fierceenergy.com/story/energy-storage-compared-2005-solar-market/2014-02-07