Stationary battery storage has evolved rapidly, and in short order, has become a crowded and highly competitive clean energy market and industry sector, not only in the U.S., but in Western Europe and the Asia-Pacific. Leading vendors, such as LG Chem, Samsung SDI, BYD, Panasonic and Toshiba, as well as GE, Tesla and others, are all competing for a dominant share of a small, but fast-growing, market.

With demand growing and manufacturing costs falling – anywhere from 40 percent to 60 percent in the last 18 months – both vendors and end users are focusing on reducing costs across the balance of the value chain, Navigant Research highlighted in a new market research report. One key focal point is energy storage systems integration (ESSI), which Navigant expects will be a key revenue driver across the full range of technologies required to extract full value from smart stationary battery storage systems.

Sanguine when it comes to ESSI business prospects, revenues for so-called enabling energy storage technologies will exhibit strong growth and reach $21.5 billion annually by 2024, Navigant said in its Energy Storage System Integrators Leaderboard Report.

Competitive Pricing, Value Propositions, Scalability

Still in an early phase of market development, customer pricing and service terms, features and options for ESSI continue to evolve at a rapid pace. Vendors are working with key early adopters to develop and try out various pricing and valuation models, even as they negotiate, bid on and close deals with utilities, commercial and industrial (C&I) companies, and government and public sector organizations.

ESSI providers need to manage complex and, at this stage, highly customized installations, while also keeping up with and demonstrating how technological innovations can be of value to customers large, mid-sized and small, not only today, but over the course of time, Navigant principal research analyst and report author Anissa Dehamna said in an interview.

While lithium-ion is the predominant advanced battery technology in the market, project developers and end users have begun to hedge their bets by investing in and deploying other types of smart battery storage technology, such as flow batteries.

Once the technology is proven in the field and at scale,

the next major concern for end users is value for money and

the ability to scale, Dehamna said. The ability to

aggregate and deliver promised value from

behind-the-meter systems distributed across multiple utility

customer sites is still unproven, for example, she noted.

“If we keep seeing very customized approaches, that will contribute to keeping prices on the higher end of the scale,” Dehamna said. “End users and developers are focused on cutting costs, or increasing value, in other words. At this stage, they don't expect to see a perfect fit technologically, but they do want to see that the technology performs as advertised and can deliver the value they expect.”

In order to be competitive, ESSI providers will have to be agile, quick, extremely competent, responsive to shifts in customer needs, and innovate at a consistently rapid pace.

“The

most successful ESSI firms will be those with the

technology, strategy and execution that permit both

competitive pricing and compelling customer value

propositions,” she said.

“The

most successful ESSI firms will be those with the

technology, strategy and execution that permit both

competitive pricing and compelling customer value

propositions,” she said.

Software Platforms, Systems Controls

ESSI software and controls are key, core elements when it comes to competition and differentiation among vendors, as it is in terms of overall systems performance and end user ease-of-use, according to Navigant.

Critical to end users managing daily operations, the software platforms offered by many of the 12 leading ESSIs that Navigant surveyed are able to virtually model a system's operations at a given end user site before the process of physically installing the system begins.

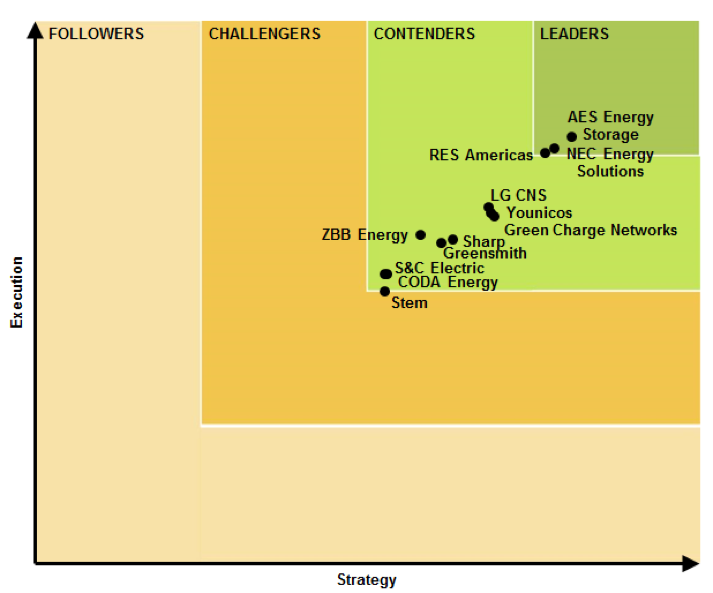

Aiming to provide end users and other market participants with insight as to the relative strengths and weaknesses of each of the 12 ESSIs, Navigant examines their strategies and ability to execute them. (See graph.)

Stationary Battery Storage Geography

Geographically speaking, there are significant differences when it comes to the nascent market for smart battery and energy storage systems, and that is primarily to due to regulatory regimes, Dehamna said.

The fastest rates of early adoption are being seen in markets where energy costs are comparatively high, there's a pressing need to integrate variable or intermittent renewable power generation capacity, or government has instituted renewable energy or energy efficiency targets.

Generally speaking, manufacturers and developers in the U.S. have focused on middle-tier C&I, government and public sector organizations as well as utilities. The market in Western Europe is focused more on distribution utilities, while market players in Asian markets have been focusing more on the residential market segment.

Graph: Navigant Research Energy Storage Systems Integrators Report

Lead image: *Solar PV – Smart Battery Storage System. Credit: Kauai Island Utility Cooperative.

© Copyright 1999-2015 RenewableEnergyWorld.com - All rights reserved